How to create a single view of the customer with banking software

Related topics:

Last updated:

Though the concept of creating a single customer view is not new for the banking industry, some CIOs still find it vague and unclear. To dispel their doubts, we’ve prepared the following article explaining how banks can create a single customer profile and which obstacles may hinder its creation.

Organization-centric software creates fragmented customer data

A typical IT architecture model implemented in most retail banks is organization-centric, which means that all banking software is built around banking products and services. For example, a retail bank may have mortgage lending software, loan origination and servicing solutions, software for customer accounts management, cards and payments processing, internet and mobile banking solutions, etc. All these banking IT solutions may store information in multiple unrelated databases.

As a result, customer information is scattered across different systems making it almost impossible to understand the entire customer lifecycle across channels and products. If banks want to maximize the value of their most valuable asset (customers), they need to move from a fragmented set of data repositories to an integrated customer-centric model based on a single view of the customer.

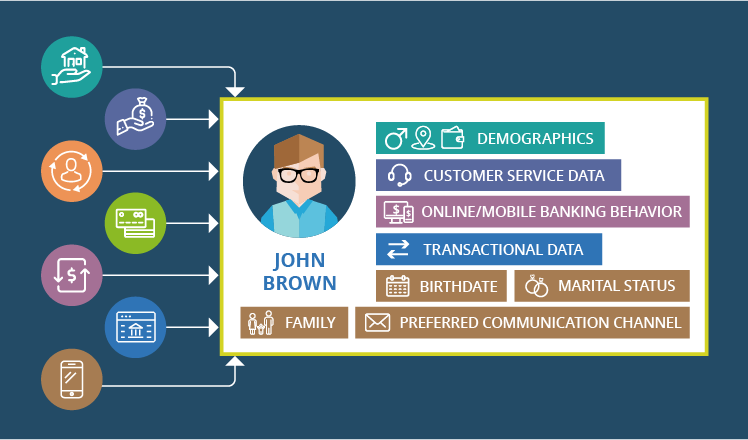

A single view of the customer allows tracing each customer’s lifecycle

A single customer view is a consistent summary of information about a bank’s customers as well as all relationships and transactions they’ve had in that particular bank.

Such information can include:

- Demographics – income, age, location, etc.;

- Data on customer service satisfaction – complaints, inquiries, praise or suggestions, etc.;

- Online and mobile banking behavior – the most frequent activities, visits history, etc.;

- Transactional data – number of monthly transactions, payment patterns, etc.

Besides, data from a banking CRM can provide more insights into customers’ purchasing habits, financial needs and life stages.

This data can include:

- Birth date

- Marital status

- Number and age of family members

- Preferred communication channel, etc.

N.B.: For a complete list of data that can be found in a CRM customer profile, have a look at this demo.

Summarizing all this information, a bank can calculate and estimate a customer’s lifetime value, identify customer segments that are likely to bring the most revenue as well as define the potential value of existing relationships with a particular customer segment (e.g., mobile banking solutions can help to meet the needs of Millennials).

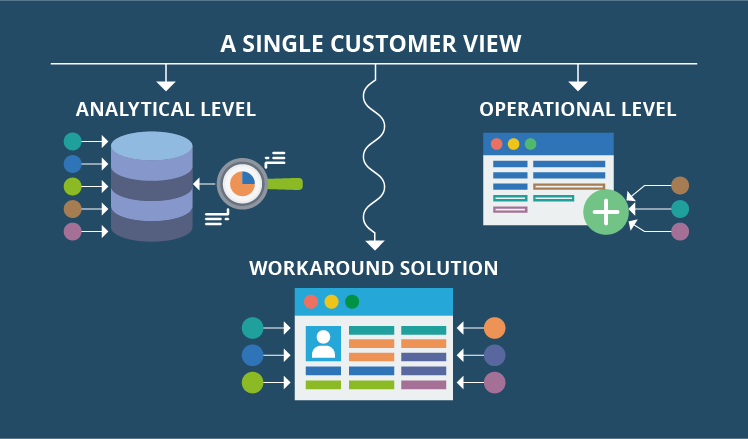

How to create a single view of the customer

A single customer view can be created at 1) analytical level and 2) operational level.

In the first case, a bank needs to gather data from the existing systems (e.g., solutions for customer accounts management, card and payment processing) to a separate data warehouse and apply banking analytics. Here, all the existing systems stay untouched, only data from their current databases is manipulated.

The operational level implies a consolidation of customer data in one system with customer information taken from other banking systems. For example, a banking CRM can be extended with additional fields that display customer service data. Since the implementation process requires modification of the existing systems, the final solution’s cost may be too high for a bank.

Still, there’s a workaround solution. A bank can create a separate application displaying customer information from several or all banking systems in a consolidated customer record. In this case, a bank needs to define data elements (or standardized customer parameters) that will be included in customer information summary and assign a particular customer ID for each customer data summary. Then, each banking software system will contain a link to that application with customer ID in parameters.

Benefits of creating a single customer view and obstacles to overcome

Achieving a single customer view can bring a number of tangible benefits for banks:

- Better risk assessment.

- Quicker and more accurate lending decisions.

- More accurate marketing offers and improvements in cross-selling activities.

- Better customer understanding and more effective product development.

- Increased efficiency of customer service agents.

However, before taking actions, a retail bank should ensure its current software has accurate customer data. Otherwise, it will need to ensure data cleansing, i.e. update obsolete customer information, remove duplicates and merge profiles belonging to the same customer.

Other obstacles may include inconsistent data formats (e.g., a phone number or address written and structured in a different manner), disparate storage locations (e.g., both in-house and outsourced systems) as well as multiple mergers and acquisitions, which significantly complicate a bank’s IT infrastructure.

Summing it up

Though the preparatory stage may take its time, the benefits of creating a single view on customers look very attractive for banks. Since the creation of an integrated customer-centric model will allow tracing each customer’s lifecycle, banking software solutions for gathering customer data may be a wise investment.