Property and Casualty (P&C) Insurance Software

Features, Development Best Practices, Costs

ScienceSoft engineers custom P&C insurance solutions that address the common drawbacks of off-the-shelf tools, such as generic panels of insurance products, limited risk and jurisdiction coverage, rigid features and data models, and predefined integrations. Our clients get secure, interoperable solutions that can quickly adapt to market and regulatory change while keeping TCO under control.

Insurance Software - ScienceSoft")

Contributors

Senior Insurance IT & AI Consultant, ScienceSoft

Lead Test Engineer and QA Consultant, ScienceSoft

Property and Casualty Insurance Software: Key Aspects

Property and casualty insurance software serves as a centralized platform for managing underwriting, policy, billing, and claims activities across P&C product lines. It provides a unified view of products, customers, and risks and often includes self-service tools for customers and producers.

- Key integrations for a P&C insurance system: CRM, insurance distribution platforms, risk data sources, payment utilities, claims execution facilitators, and more.

- Implementation time: around 3–6 months for specialized components and tools; 8–16 months for the core modules of a full-scale system.

- Development costs: $150,000–$600,000 for a specialized component; $300,000–$1,000,000 for a task-specific solution; $1,000,000–$3,500,000+ for a multi-functional system. Use our free calculator to estimate the cost for your case.

- Major financial outcomes: reduced operational costs, improved loss ratios, uplift in business profitability.

Why Half of the US P&C Insurers Opt for Custom Software

A 2025 McKinsey report found that roughly half of US P&C carriers choose to build custom insurance solutions from scratch or expand the commercial suites they use with custom components. From ScienceSoft’s experience, P&C insurance market participants often prioritize custom development to overcome the challenges they commonly face with off-the-shelf software products:

- Limited flexibility of generic suites for implementing organization-specific underwriting rules, rating algorithms, claims handling paths, renewal scenarios, and data architectures. Ready-made solutions typically enforce predefined rules and analytics models that are difficult to fully adapt to unique servicing processes.

- Lack of support for complex and niche product portfolios, specifically, commercial and personal specialty lines, liability products, and alternative insurance models that typically require highly specific automation features.

- Difficulties in integrating off-the-shelf software with legacy internal tools, specialized data platforms, local regulatory systems and vendor networks, and modern payment rails.

- Challenges in aligning OOTB platforms with jurisdiction-specific operational regulations, such as NAIC model laws adopted at the state level, state DOI requirements for cancellation and non-renewal notice periods, and state-specific underwriting constraints (e.g., California’s Proposition 103, Florida’s property insurance notice requirements).

- Slow adaptation of commercial platforms to the insurer’s new business rules, coverage models, insurable asset classes, risks, and regulatory mandates. Some product vendors may choose not to adapt to certain market changes at all.

- Limited support for tailored automation setups powered by artificial intelligence (AI). Pre-built insurance software may not allow training traditional AI models on proprietary datasets and implementing tailored generative AI pipelines (e.g., retrieval-augmented generation), which limits model access to the entity’s contextual data and, as a result, hampers output accuracy.

Legacy custom cores rarely require a from-scratch rebuild

Many P&C insurers see custom engineering as the only way to upgrade their old home-grown systems. However, a complete rebuild from scratch is rarely justified. In most of ScienceSoft’s P&C software projects, we retained the legacy core and added custom modules for specific tasks. This is the fastest and cheapest way to introduce modern automation and line-specific features without sacrificing customization depth. Yes, it may require technical enhancements and new integrations, but it’s still far more economical than a ground-up overhaul.

If a custom platform struggles with performance, a focused revamp of selected components can be enough to unlock value. In one case, we helped a P&C carrier double the efficiency of its custom insurance management system by only resolving code-level and database issues.

A full rebuild is necessary only when the system’s architecture and underlying technology fundamentally limit scaling, integrations, and feature extension. To put this into perspective, the last time we had to complete full replacement, the carrier’s core system was entering its third decade, built on an architecture that had lost its edge before the microservices concept even emerged. Even then, we prioritized phased modernization with gradual component replacement and retained all viable system parts to optimize costs.

Major ROI Drivers for Property and Casualty Insurance Solutions

P&C insurers report impressive gains from their custom systems. A recent study from Deloitte showed that, in claims alone, workflow automation enabled by tailored P&C software can reduce operational costs by up to $40 million for large carriers, with total savings of up to $80 million over five years after software launch.

Drawing on previous P&C insurance software projects and proprietary research, ScienceSoft’s consultants forecast the following results from custom software implementations for mid-sized and large P&C carriers over a three- to five-year period:

P&C Insurance Lines to Automate With Custom Software

These are some of the traditional and alternative P&C insurance lines ScienceSoft engineers specialized software for:

Personal P&C lines

- Personal auto and motor insurance

- Homeowners insurance

- Renters and condo insurance

- Personal property insurance

- Personal umbrella insurance

Commercial P&C lines

Alternative P&C models

- Usage-based auto insurance

- Parametric insurance

- Embedded insurance

- Microinsurance

- Peer-to-peer insurance

- Commercial self-insurance

- Captive insurance

Functionality of P&C Insurance Software

Below, ScienceSoft’s consultants share a comprehensive map of modules that can be included in P&C insurance solutions. Depending on your needs and existing tech stack, we can build a multi-task P&C insurance platform or add custom modules across specific insurance functions.

![]()

P&C insurance product management

Product teams can onboard new products using customizable templates and link them to the dedicated operational policies and automation rules (rating, underwriting, claim handling, etc.). Custom systems let users configure tailored coverage structures by insurance line, distribution channel, region, and more. They can automate product change workflows, including approval routing and compliance checks. Custom solutions can also include scenario modeling and what-if analysis tools so insurers can simulate the impact of changes in specific product attributes before updates go live.

![]()

P&C insurance systems provide a centralized, version-controlled repository for insurance policies, policy lifecycle data, and product-specific policy configurations. Policy administrators can create custom templates for policy documents using a no-code template editor or apply unified forms (e.g., ACORD for certificates of insurance). The software automates policy issuance, change, renewals, and cancellations based on user-defined endorsement logic. Custom solutions can automate complex P&C policy workflows, e.g., bundle policies and apply cross-policy discounts for shared insured property.

![]()

Custom P&C underwriting engines can automatically aggregate insurance applications across distribution channels and extract applicant, asset, and risk details. They can match applicants' data against the organization's systems and trustworthy external sources, spot gaps, and trigger requests for missing evidence, and quantify risks based on the organization’s proprietary risk scoring formulas. Underwriters can set up risk-based automation thresholds so the engine can underwrite standard cases right away while routing complex risks for manual review.

![]()

Rating and pricing

Users can apply proprietary rate tables, rating algorithms, discounts, surcharges, and coverage dependencies to produce personalized P&C premiums. The system automatically recalculates premiums during endorsements, renewals, and mid-term coverage adjustments using up-to-date rates. Custom pricing engines can handle complex line-specific logic (e.g., protection class/cat loads, fleet behavior discounts, scheduled-property aggregation) and support dynamic premium calculation models, e.g., for usage-based vehicle insurance programs.

![]()

Billing and accounting

P&C insurance systems can automate invoice generation, installment scheduling, payment reconciliation, collections, and bookkeeping across policy, claims, and commission transactions. Carriers can apply firm-specific payment plans, commission settlement models, down-payment rules, and refund logic for mid-term cancellations and rewrites. Custom software can accommodate non-standard chart-of-accounts structures, jurisdiction- and line-level books, and specialized workflows, e.g., expense reallocation across the insurer’s personal and commercial portfolios.

![]()

P&C insurance platforms can automate the entire claim lifecycle, from FNOL intake to closure. They validate claimed coverage against policy terms, apply deductibles and limits, and triage claims based on date and severity. Depending on case complexity, claims engines can approve claims automatically or route them to adjusters for manual handling based on location and workload. Custom systems let insurers and third-party administrators configure proprietary claim segmentation models, handling paths, and limit-based authorizations for straight-through settlements.

![]()

Reinsurance management

Reinsurance modules in P&C core insurance software automate ceded premium calculation, claim allocation, and recoverables tracking across proportional and non-proportional structures. They can match policies and claims to treaty terms, generate bordereaux and reinsurer reports, and update treaty-based allocations and bordereaux as exposure and claims data changes. Custom solutions can handle insurer-specific workflows across facultative placements, occurrence-based catastrophe aggregation, and attachment point calculation.

![]()

P&C risk engines continuously calculate exposure and concentration metrics across insurance accounts, portfolios, insured locations, perils, and coverage limits. They spot growing and abnormal exposures, notify underwriting, actuarial, and portfolio teams, and can trigger risk mitigation workflows, e.g., underwriting restrictions or portfolio rebalancing. Insurers can implement proprietary risk governance logic, define capacity thresholds by specific peril and geography, and set non-standard triggers for reinsurance workflows.

![]()

In underwriting, fraud detection engines flag inconsistencies in applications and trigger bind restrictions until review. In claims, they detect suspicious claims and generate fraud alerts for SIU, supported by risk scores and evidence trails. Claims fraud tools can also create SIU cases, assign investigators, trigger temporary claim handling restrictions, and enforce disbursement hard stops. Custom systems can be designed to automate the carrier’s tailored fraud investigation playbooks across specific types of P&C fraud, e.g., car fronting, staged collisions, or contractor abuse.

![]()

P&C insurance platforms can calculate and track organization-specific KPIs across underwriting, claims, billing, distribution, portfolio risk, and finance. They analyze variance and flag deviations that require corrective action. Role-specific analytical dashboards provide insurance teams with aggregated and drill-down views and multidimensional slicing options (by product, jurisdiction, peril, and more). Custom systems can accommodate proprietary insurance analytical models, including machine learning (ML) models for diagnostics, predictive, and optimization tasks.

![]()

Agent and broker workspaces

Agents and brokers can submit and track applications, generate branded quotes from ACORD files, bind policies within delegated authority, and service policies end-to-end using dedicated insurance portals. Custom portals can automate policy renewal alerts, cross-sell prompting, hit ratio and commission tracking, and compliance checks (agent licensing, product eligibility restrictions, etc.). They can include interactive agent training modules and user self-education sections. Agents and brokers can collaborate with carrier teams in real time via a live chat.

![]()

Customer self-service options

Self-service portals and apps allow P&C policyholders to view active policies, pay premiums, update contact and billing details, request policy changes, submit claims, and track claims processing status. Custom portals and apps can accommodate tailored automation capabilities, forms, notifications, authentication options, and assistive features. Custom solutions can include value-adding features like vehicle damage self-description using 3D models, criteria-based search of loss handling vendors, and 24/7 user support by AI chatbots.

![]()

Compliance management

Custom compliance engines can be designed to support both general frameworks (e.g., federal AML/OFAC requirements) and local regulations, such as state-level DOI and NAIC model law enforcement and state-specific underwriting constraints. Compliance teams can track breaches across rate usage, underwriting decision-making, cancellation notice timelines, claims settlements, and other areas. The software can compose regulatory report packages, including market conduct evidence trails and DOI extracts.

![]()

Data governance and security

Custom P&C insurance platforms can be built in compliance with the requirements of carriers and regulators (NAIC, SOX, NYDFS, CCPA, GLBA, GDPR, and more). The software applies role-based access controls, multi-factor authentication, and data encryption and maintains a full log of user activities. Custom security layers allow insurers, intermediaries, and service providers to implement fine-grained, business-specific controls, such as restricting employee access to certain documents and enforcing state-based data residency rules.

How AI Can Reinforce Property and Casualty Insurance

Intelligent automation is steadily gaining traction among P&C insurers, with 70% of domain players already using AI for at least one core function, and 86% planning to increase AI spending in the near term. Early results drive the demand forward: insurers report results such as a 110%+ increase in underwriter productivity, 58x faster claim reviews, and 70%+ automation rates across customer servicing operations.

ScienceSoft can extend P&C insurance management software with the following capabilities:

![]()

P&C insurance systems can employ large language models (LLMs) to automatically process complex applications and claims. LLMs can parse multi-format submissions (ACORD forms, broker emails, loss runs, inspection reports, etc.), extract case and risk attributes, and generate summaries for underwriters and adjusters. They can spot inaccuracies and detect document manipulation and fraud. For example, in claims, LLMs can reconstruct timelines of loss events, identify inconsistencies between reported facts and policy terms, and flag suspicious narrations.

![]()

Insurance specialists can ask GenAI assistants to find relevant data, assemble tailored briefs and reports with linked evidence, and draft compliant customer communications. Copilots can explain coverage applicability, deductible impact, premium calculations, and other insurance concepts, helping teams communicate product logic to agents and customers. They can also suggest optimal, context- and compliance-aware steps for handling insurance tasks. Explainable AI techniques (e.g., SHAP, LIME) ensure transparency of the logic behind intelligent suggestions.

![]()

Agentic automation of P&C insurance workflows

AI agents can monitor policy, underwriting, billing, claims, and compliance events across operational systems, collect required data from internal and external sources, and trigger downstream actions for routine cases. For example, following FNOL, a claims AI agent can validate coverage, collect supplementary risk data, run call-based claim verification, assign a handler, and prepare an audit-ready activity log. Rule-based guardrails and human-in-the-loop controls are applied for safe and accountable automation.

![]()

Tailored machine learning (ML) and deep learning models can be applied to analyze policy attributes, claim development patterns, external hazards, and financial metrics and predict time-framed risk and finance trends. Model outputs can trigger preemptive actions, e.g., enhanced underwriting review, manual claim investigation, reserve adjustment, or capital reallocation. P&C insurance systems should incorporate drift monitoring, bias detection, and explainability mechanisms to support model risk governance.

See P&C Insurance AI in Action

Watch Vadim Belski, ScienceSoft’s Head of AI, try to make a “fraudulent claim” for homeowners' coverage and get caught by the AI agent. According to ScienceSoft’s consultants, the agentic AI solution can boost investigator capacity by 40% and drive 20%+ higher fraud detection rates through sentiment-based fraud indicators.

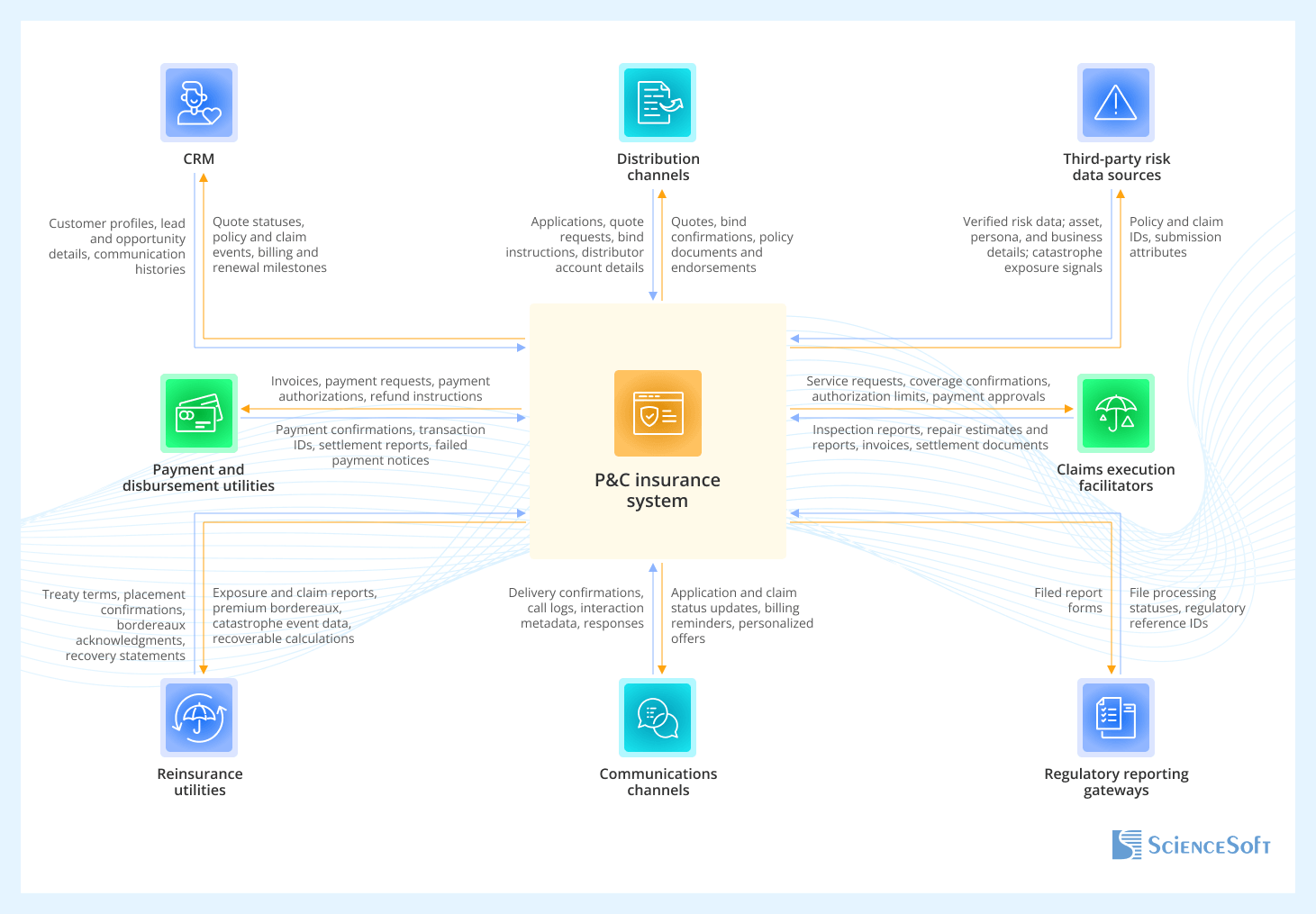

Important Integrations for a Property and Casualty Insurance System

CRM

Custom platforms or popular enterprise CRMs (e.g., Salesforce, Microsoft Dynamics 365).

To provide front-line and back-office teams with a unified customer view, auto-populate documents with customer data, and trigger customer interactions (quote follow-ups, renewal outreach, cross-sell offers).

Distribution channels

The insurer’s website, agent and broker networks, MGA portals, insurance marketplaces, etc.

For faster quote-to-bind cycles, straight-through application processing for personal lines, and streamlined broker workflows across commercial accounts.

Third-party risk data sources

Loss databases (e.g., CLUE), asset tracking systems (telematics, utility, property occupancy, geocoding), geospatial and weather data platforms, ID databases, KYC and open banking services, fraud databases (e.g., NICB), and more.

To enrich customer and asset profiles with external risk evidence; to quickly gather data on catastrophic hazards.

Payment and disbursement utilities

Payment gateways, bank systems, disbursement networks (ACH, push-to-card, e-check), etc.

To automate premium collection and claim disbursement, track real-time payment progress, and accelerate reconciliation.

Claims execution facilitators

E.g., field inspection and adjuster platforms, repair and restoration vendor networks, attorney and litigation provider systems.

For streamlined vendor coordination, automated tracking of service status, and quicker exchange of claim handling documents.

Reinsurance utilities

Reinsurers’ systems, bordereaux exchange tools, treaty placement platforms.

To speed up reinsurance requests and report claims, portfolio risks, and catastrophe events to reinsurance partners faster.

Communications channels

Email, SMS, and messaging services, call center systems.

To automate customer and partner communications across the P&C insurance lifecycle and enforce timely statutory notifications.

Regulatory reporting gateways

E.g., state DOI reporting channels, SERFF filing platforms.

For automated submission of regulatory reports and simplified submission status tracking.

Best Practices for P&C Insurance Software Development

Below, ScienceSoft’s experts share their best practices for engineering reliable and cost-effective P&C insurance software solutions.

![]()

The solution should be planned around integrations from day one

In ScienceSoft’s projects, the architects commonly apply an API-first design, where integrations are planned before solution features. Even if you build only one software module, this approach helps ensure interoperability with internal and external systems and avoids costly workarounds later on. Defining a common data model for key entities (policy, asset, risk, payment, etc.), standardizing how they are represented in APIs, and applying API versioning helps evolve the entities and APIs over time without breaking existing integrations.

For a multi-functional system, you could consider implementing integrations via a dedicated orchestration layer with API gateways and an event bus. Such a design lets you avoid embedding connectors into every module, easily swap software vendors and add new data sources, and run phased modernization programs without rebuilding integrations.

![]()

Logic and performance tests should reflect real P&C insurance workflows

Testing on the insurance organization’s real data or synthetic datasets that closely mirror production data confirms that the software will remain stable, accurate, and compliant once set live. QA engineers at ScienceSoft stress that “happy path” testing scenarios alone won’t show defects in specialized, exception-heavy P&C insurance workflows. Including exceptions, corner and edge cases, risk change paths, catastrophe conditions, and varying service and compliance rules in a functional testing data panel helps ensure adequate logic validation.

Performance testing should follow the same principle. Load tests must simulate mass policy renewals, billing cycle peaks, end-of-period reporting runs, and catastrophe events with sudden FNOL surges. This way, you can validate software performance under the operational conditions most likely to cause system breakdowns, delays, and SLA breaches.

Establishing continuous performance testing is a wise move to protect your operations when things go live. ScienceSoft’s P&C client Brush Claims was smart to set up continuous testing and monitoring pipelines for its claims suite and involve our engineers to fix issues as soon as early warning signs appeared. This proactive step helped Brush Claims smoothly handle a surge in P&C catastrophic claims when hurricanes Helene and Milton hit in 2024. Without timely performance enhancements, their software would likely stall on day one of the catastrophe.

![]()

AI should be brought in only when a robust data foundation is in place

In practice, this means preparing data and systems for AI rollout before engineering the AI solution itself. The first step is orchestrating policy, claims, exposure, finance, and servicing data into unified datasets with clear ownership. This is required to ensure that AI-generated insights draw on a single, consistent source of truth. Data lineage and robust data quality controls are equally important because you must be able to trace which records influenced AI outputs and prove decision accuracy and validity to regulators, customers, and internal stakeholders.

ScienceSoft’s engineers implement automated data integration, validation, and governance pipelines to streamline these processes. Consolidating data into centralized storage (typically a data warehouse for structured and semi-structured data and a data lake for unstructured files) simplifies governance and makes enterprise-wide data accessible for AI-supported workflows.

For LLM and GenAI capabilities, you also need specialized RAG components, such as metadata tagging tools, data vectorization pipelines, and vector stores. These components enable LLMs to access and interpret the insurance organization’s unstructured proprietary data. LLM platforms by major cloud platforms (e.g., Microsoft’s Azure AI Foundry, AWS’ Amazon Bedrock) provide ready-to-use RAG tooling, so you don’t need to build these components from scratch.

Costs of Property and Casualty Insurance Solutions

Developing property and casualty insurance software may cost from $150,000 to $3,500,000+, depending on the solution’s functionality, the scope of supported product lines and jurisdictions, the number and complexity of integrations, as well as performance, scalability, and security requirements.

Here are ScienceSoft’s sample cost ranges for common P&C solution types:

![]()

$150,000–$600,000

A task-specific software component (e.g., for P&C data consolidation, third-party platform integration, intelligent automation of insurance workflows, or smart customer assistance) built on top of the insurer’s existing core system.

![]()

$300,000–$1,000,000

A custom solution that automates a specific insurance function (e.g., underwriting, claims, policy administration). We can implement it as a module in the core platform or as a standalone tool integrated with other systems.

![]()

$1,000,000–$3,500,000+

A large-scale custom system that handles the entire scope of P&C insurance activities, from product design and application processing to operational analytics and regulatory reporting. The system provides role-specific interfaces and tools, and supports both traditional and AI-driven automation.

Wondering how much your P&C software project will cost?

Use our online calculator to describe your needs, and we'll get back to you shortly with a tailored estimate. It’s free and non-binding.

* The estimates are for mid-sized insurers (<2,000 employees) serving 1–5 traditional P&C lines. The final implementation cost will depend on the insurer’s specific needs, the maturity of the firm’s IT ecosystem, and the complexity of data migration procedures.

Why Develop P&C Insurance Software With ScienceSoft

-

Since 2012 in engineering custom software solutions for the insurance industry.

- Insurance IT and compliance consultants (NAIC, NYDFS, CCPA, GDPR, etc.) with 5–20 years of experience.

- 45+ certified project managers (PMP, PSM I, PSPO I, ICP-APM) who succeeded in large-scale projects for Fortune 500 firms.

- Principal architects with hands-on experience in designing complex insurance automation systems and driving secure implementation of advanced technologies.

- 350+ software engineers, 50% of whom are seniors or leads.

- Established practices to ensure the high quality of insurance solutions and their delivery on the agreed timelines and budget, despite project constraints or uncertain requirements.

Our Clients Share Their Experience With ScienceSoft

ScienceSoft are responsive, technically sharp, and they communicate well with our people. When we've needed to move fast, they've stepped up and delivered. What I appreciate most is their proactive approach. They don't just wait for us to identify issues. They bring solutions to the table and help us prioritize what matters most. That kind of partnership is hard to find.

ScienceSoft demonstrated a deep understanding of our requirements, and their insurtech developers needed minimal supervision.

What stood out was ScienceSoft's proactive suggestions for cost-saving architecture design and tech stack solutions. Their input ensured we stayed within budget without compromising on software quality. The value we derived from partnering with ScienceSoft is definitely worth the investment.

Partnering with ScienceSoft has been an excellent experience. Their team transformed our underwriting platform into a well-oiled machine. They identified and fixed several longstanding issues that had been causing us persistent difficulties. Their communication was exemplary; unlike our previous experiences with outsourcing, we never had to chase them for updates, and they were always prompt in responding to our queries.

Damien Sewell

Head of IT Projects

ScienceSoft’s quick buy-in and readiness to take the initiative made the project faster and less stressful for everyone involved, from Capital IM’s insurance specialists to leadership. At the end of a short yet highly productive two months, we got a secure and wholly owned property insurance solution that is fully adapted to Capital IM’s corporate practices and brand book. We couldn’t have asked for a better IT partner.