Q2 2026 Insurance AI Trends: Assistive AI Outpaces Agentic AI in Enterprise Deployments, Market Players Invest Heavily in AI Scaling Infrastructures

Related topics:

5 min read

Last updated:

Insurance market participants are moving toward autonomous AI automation solutions, yet adoption remains focused on copilot assistants. Drawing on ScienceSoft’s Q2 2026 Insurance AI Market Watch and 14 years of experience in insurance AI transformation, we outline where AI is delivering the biggest value now, what insurance organizations and vendors should prepare for next, and how legacy infrastructures and regulations will shape the 2026 AI journeys.

At a glance:

- The industry’s AI investments are growing. Insurance organizations are raising AI budgets, and AI-focused startups are attracting a record share of insurtech funding, signaling strategic confidence in AI’s value.

- Assistive AI is becoming the dominant deployment model. Most newly launched insurance AI solutions focus on assisting producers and customers with coverage selection, quoting, and claim handling.

- Agentic AI adoption remains measured. While technology vendors are pushing multi-task and specialty agents, insurers focus on guardrails and governance before deploying autonomous AI capabilities.

- Legacy systems and regulatory complexity constrain AI adoption. Infrastructure readiness, practical integration paths, and robust governance are becoming imperative for organizations seeking to scale AI.

AI Terms Used in This Article

Assistive AI (e.g., chatbots, copilots, voice assistants) helps employees or customers by retrieving information, summarizing documents, drafting communications, and recommending next steps. A person still reviews the output and makes the decision.

Agentic AI uses generative AI and workflow automation to complete predefined process steps, such as assembling a document package, processing an application, or routing a claim. It requires stronger controls because it can perform multi-step actions with only limited human involvement.

Traditional machine learning (non-generative AI) is still widely used for prediction-heavy insurance tasks, such as risk scoring, fraud detection, claim severity forecasting, and pricing support.

Insurance Outpaces Other Industries in AI Adoption, Prompted by Customer Expectations

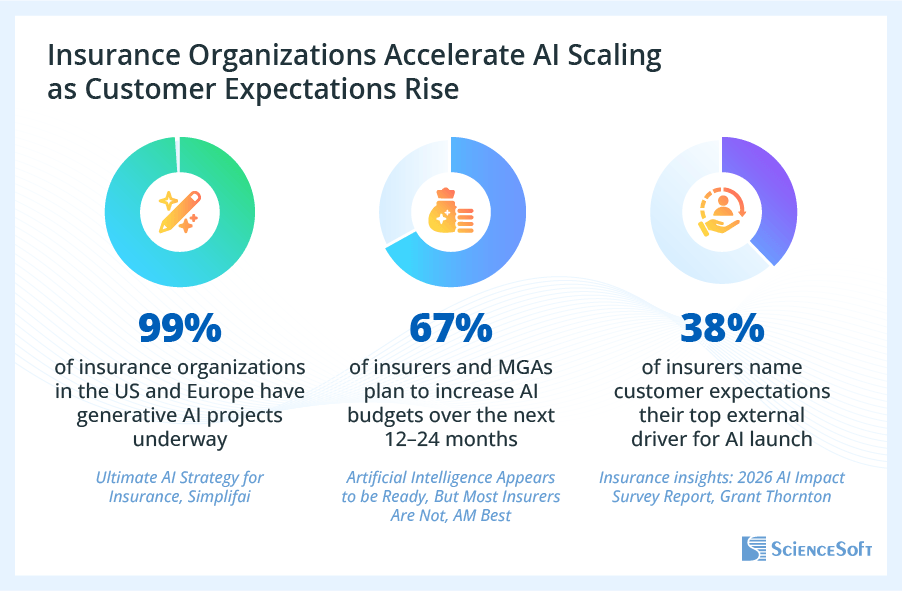

In Q2 2026, insurance remained one of the most aggressive adopters of AI among industries. A 2026 research by Simplifai found that 99% of insurers in the US and Europe now have generative AI projects underway. The 2026 AI Impact Survey by Grant Thornton shares that 62% of insurance organizations are currently scaling AI initiatives across multiple functions — 13% above the cross-industry average. According to the same report, 52% of organizations report revenue growth attributable to AI use, exceeding the cross-industry average by 15%.

Large insurers led AI adoption. Research from Datos Insights, published in April 2026, indicates that large carriers are moving beyond isolated use cases toward enterprise-wide AI capabilities. Nearly 80% have implemented some AI-assisted or autonomous processing workflows, and roughly 50% have deployed AI solutions spanning multiple business functions. Midsize insurers are progressing at a slower pace, with 67% reporting autonomous processing initiatives and few working on cross-functional AI programs.

Insurance organizations name customer expectations the primary catalyst for AI adoption. In the same survey by Grant Thornton, 38% of insurance leaders cited customer demand as the biggest external driver of AI adoption. Insurance incumbents have historically lagged behind other BFSI players in digital customer satisfaction. Consultants at ScienceSoft observe that many insurers are now turning to AI to address long-standing customer expectations for faster service, more personalized interactions, and smoother policy and claims experiences.

Consumer attitudes appear to be evolving accordingly. Insurity's 2026 survey of more than 1,000 US consumers found that support for insurers' use of AI nearly doubled year-over-year, increasing from 20% in 2025 to 39% in 2026.

However, the survey’s findings also reveal clear boundaries regarding consumer trust. While 46% of consumers are comfortable with insurers’ use of AI automation for routines like quote generation, only 16% would trust AI to decide on premiums and policy renewals. Similarly, acceptance is low for customer representation authority: while 39% of consumers would use AI to track submission statuses, only 22% would let AI file claims on their behalf.

Budgeting patterns reflect insurance organizations’ plans to accelerate AI adoption. According to the 2026 report by AM Best, 67% of insurers and managing general agents plan to increase AI spending over the next 12–24 months. Simplifai found that 83% of large carriers in the US and Europe currently allocate at least $5 million annually to AI.

Investors’ sustained confidence in AI value creates momentum for AI scaling across the broader insurance technology landscape. Gallagher Re's Global Insurtech Report shows that 95.2% of insurtech funding in Q1 2026 flowed to AI-focused firms, up from 77.9% in Q4 2025. Average deal size reached $23.23 million; the highest level recorded since Q4 2021.

Enterprise Deployments Focus on Assistive AI for Insurance Customers and Producers

While discussions around autonomous AI continue to attract attention, the majority of production rollouts announced during Q2 2026 focused on assistive AI. In this model, AI retrieves and summarizes data, drafts documents and communications, and provides recommendations that help insurance professionals and customers act more efficiently. Humans remain responsible for instructions, decisions, and actions.

The growing focus on non-carrier AI use cases ScienceSoft observed in Q1 2026 in the insurtech space continued through Q2 across insurance organizations. The quarter's most notable AI rollouts centered on specialized AI assistants for producers and customers.

Product selection and quoting emerged as the primary AI assistance areas. State Farm implemented several assistive capabilities aimed to enhance advisory and quote-related interactions between customers and agents. Its Household Story copilot summarizes customer cases, analyzes coverage gaps, and recommends relevant products, enabling agents to deliver more personalized advice. Navi, another AI assistant for agents, can retrieve application details and generate quotes in minutes, reducing agents’ manual effort.

Liberty Mutual Insurance introduced assistive AI directly into customer acquisition by launching an auto insurance quoting application within ChatGPT. The solution enables consumers to receive personalized quotes through chat-based conversations, without filling out traditional online forms. It connects directly to Liberty Mutual’s rating engine to generate actual quotes. As of Q2 2026, conversational AI quoting from Liberty Mutual Insurance was available in seven US states, and the company plans to expand it to more than 40 states by the end of Q4 2026.

Claims also remained a major area of AI assistance. Travelers expanded its e-CARMA claims risk management platform with Claim Insights, an AI-powered conversational assistant for commercial insurance customers, brokers, and agents. The assistant helps business customers and producers analyze claims portfolios, identify priority cases, compile claims packages, and track settlement statuses. By helping organizations focus on high-impact claims, the tool enables faster claim responses and stronger case oversight.

Brokers similarly deployed AI to augment advisory services. The Baldwin Group announced its enterprise partnership with Anthropic to transform company-wide operations through AI. Initial use cases focus on AI assistants helping brokers synthesize data, analyze client risks, and generate tailored product recommendations. Consultants at ScienceSoft note that Baldwin's broader AI strategy illustrates a common industry pattern: organizations first pursue productivity-enhancing copilots, then expand into autonomous workflows.

Software product vendors accelerated this trend by embedding assistive AI directly into core insurance platforms. In Q2 2026, BriteCore expanded its core suite with specialized AI copilots for underwriting, rating, billing, claim processing, document management, business rule management, and reporting. BriteCore claims its submission intake copilot alone can reduce manual intake routines by 80–90%. The company announced its plans to evolve from assistive AI toward multi-agent, orchestrated insurance workflows.

Vendors Race Toward Agentic AI. Insurers Move Cautiously

Although assistive AI dominated production deployments, Q2 2026 demonstrated growing momentum around agentic AI. Unlike assistive systems, AI agents can take actions, orchestrate multi-step workflows, and make decisions within predefined parameters with minimal human oversight, enabling a greater degree of operational autonomy.

However, the quarter's announcements reveal that agentic AI rollouts are currently being led primarily by insurtech vendors rather than insurance market participants. This market dynamic suggests that vendor offerings are advancing faster than most insurance organizations' readiness to deploy autonomous systems.

One notable insurtech release came from Duck Creek. The vendor launched Agentic AI Platform, the software product that enables insurers to deploy, orchestrate, and monitor AI agents across the insurance lifecycle. It currently offers two agentic experiences. Agentic Underwriting Workbench uses coordinated agents to intake, enrich, and triage submissions. Agentic First Notice of Loss (FNOL) applies niche agents to capture, validate, and route claims across digital and voice channels.

Notably, in Q2 2026, vendors started expanding agentic AI into specialty insurance lines. For example, DeNexus launched DeRISK UWA Agentic, an agentic underwriting platform designed specifically for industrial cyber insurance. The solution orchestrates five specialized agents to retrieve data from multi-format documents, profile and score risks, generate expected-loss estimates, and suggest premiums, policy extensions, and binding conditions. In DeNexus’ controlled pilots, its agentic platform managed to transform fragmented submission materials into underwriting-ready files within 10–20 minutes.

Right now, I wouldn’t advise most insurers to start their AI programs with agentic AI. The faster and safer route is assistive AI, which is typically easier to implement and still lets humans make the final call. But this doesn’t mean you need to wait years before you’re ready for agentic AI.

In our projects at ScienceSoft, we usually recommend phased adoption. Start with one employee-facing assistant and use it to learn how to monitor AI quality, control outputs, and measure impact — for example, underwriting speed or claim handling time. Then, once you have established governance, user trust, and executive buy-in, you can add AI agents to high-volume workflows that can be automated with relatively low risk. This would usually be submission intake, data validation, claim triage, internal case routing, and document package preparation.

Complex multi-agent AI setups become useful when the problem is not one isolated task, but the slow handoffs around it. In that case, I’d first map where people now chase information, wait for approvals, or lose context between systems. Then decide which steps AI can perform, which steps AI can only prepare for human review, and where it must stop completely. Without that clarity, multi-agent AI just automates a messy process and makes it even harder to see who is accountable.

Senior Insurance IT & AI Consultant, ScienceSoft

Traditional Machine Learning Dominates in Risk Analytics. Large Brokers Lead the Q2 Rollouts

While assistive AI and agentic AI captured much of the industry's attention during Q2 2026, traditional machine learning (ML) remained the dominant technology for risk analytics.

Unlike large language models (LLMs), which excel at interpreting unstructured data and generating content (generative AI), traditional machine learning models work best for quantitative forecasting, risk modeling, and financial optimization. Consultants at ScienceSoft highlight that insurance organizations have been deploying ML across these tasks for years and continue to invest in ML-powered predictive analytics because these capabilities remain foundational to their business profitability.

In Q2 2026, major launches of ML-supported risk intelligence platforms came from large brokers. Gallagher implemented an intelligent risk management platform, Gallagher Blueprint. The platform relies on ML-powered analytics to score customer risks, compare risk portfolios against industry benchmarks, and identify opportunities to improve insurance programs and risk management strategies.

Some brokers expanded the application of ML-powered analytics into client-side risk management. Marsh Risk launched Risk Companion, an intelligent risk management suite for its commercial insurance customers. The solution relies on machine learning engines for insurance scenario and risk modeling, outcome forecasting, and captives’ performance analysis and benchmarking. Marsh Risk suggests that the comprehensive analytics enabled by ML will help their customers better identify, measure, and mitigate risks and make more informed insurance buying decisions.

Legacy Tech Stacks and Evolving Regulations Remain the Biggest AI Adoption Barriers

Legacy core systems and infrastructures remained the insurance industry's biggest obstacle to launching and scaling AI. A recurring theme across Q2 2026 market surveys, industry conferences, and executive interviews was that legacy core architectures limit data accessibility, complicate AI integration, and constrain consistent AI scaling across insurance functions.

Research from Datos Insights highlights the scale of this challenge: 100% of insurers surveyed ranked core system modernization among their top three technology priorities for 2026. More than 50% of large insurers and 35% of midsize insurers said they plan to replace their current policy administration systems in 2026.

Consultants at ScienceSoft note that the technical patterns for integrating AI with legacy cores are increasingly becoming available, but insurers often lack the infrastructure to implement them. Layered integration architectures, like the one ScienceSoft demonstrated at the Insurance Tech & Innovation Conference 2026 in Chicago, now allow organizations to deploy AI without redesigning their current platforms. Yet, the infrastructure capabilities needed to support AI integration at scale, such as model monitoring, explainability, prompt and output controls, human-in-the-loop oversight, enterprise AI governance, and rule-based safeguards, remain underdeveloped across much of the industry.

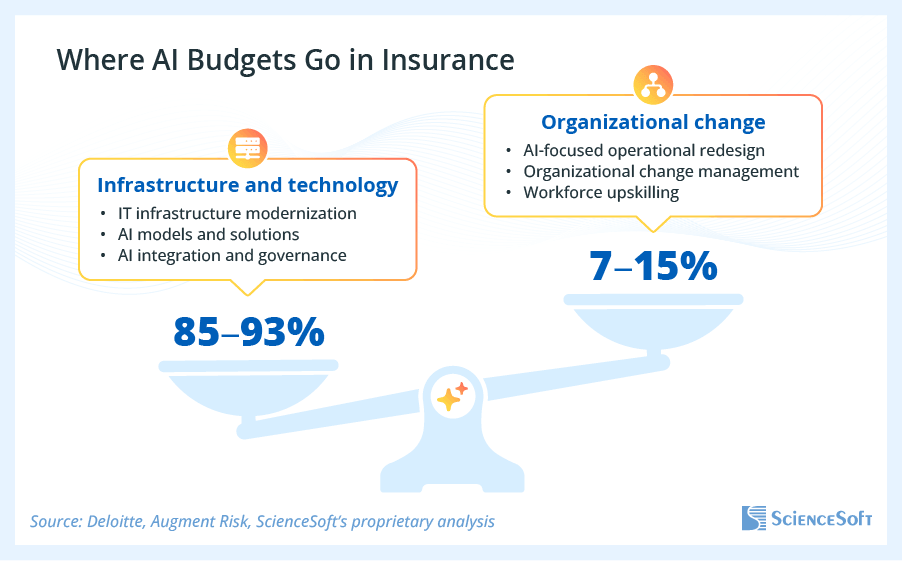

The breakdown of the sector’s AI spending also suggests that legacy infrastructures represent the primary bottleneck. Speaking at Insurtech Insights USA 2026, Grant Donkervoet, Associate Partner at Augment Risk, noted that insurers currently direct 93% of their AI budgets to upgrading IT infrastructure. Donkervoet's estimate aligns with a broader trend Deloitte has recently observed across industries: companies allocate approximately 93% of their AI budgets to technology and only 7% to workflow redesign and workforce adaptation.

Another major barrier to AI in Q2 2026 was regulatory scrutiny. In a survey by Grant Thornton, 56% of insurance organizations named regulatory compliance concerns as their biggest obstacle to deploying and scaling AI.

ScienceSoft suggests that these concerns stem from the increasingly formalized AI regulations. As of June 2026, 25 US jurisdictions had adopted the NAIC AI Model Bulletin, and 4 states established their own requirements for AI transparency, fairness, and oversight. Insurance organizations must also consider broader frameworks, such as the NIST AI Risk Management Framework, ISO/IEC 42001, and, where applicable, the EU AI Act. As a result, deploying AI prompts organizations to first invest in specialized AI governance frameworks, which delays AI rollouts and consumes project budgets.

Software product providers prioritized integrations and governance in Q2 2026 to address the industry's major concerns. Duck Creek equipped its Agentic AI Platform with ready-to-go agent orchestration capabilities, reusable compliance and governance control layers, and prebuilt integrations with popular core platforms to help insurance organizations safely operationalize AI. Similarly, BriteCore powered its AI copilot offering by AI-specific governance mechanisms, data management tools, and go-to MCP connectors for copilot integration with insurers’ policy, billing, claims, document, and workflow design systems.

Today's investment priorities reflect where the industry is in its AI maturity journey. Most insurers still need to modernize data architectures, establish governance, and build secure integration layers before they can scale AI. As a result, it's natural that infrastructure currently absorbs the majority of AI budgets.

However, infrastructure is only an enabler. AI creates business value when organizations redesign how work is performed: rethink core workflows, redefine employee responsibilities, establish new decision-making models, and prepare the workforce to collaborate with AI. These activities receive a much smaller share of investment today, yet they ultimately determine whether AI remains a collection of productivity tools or becomes a driver of enterprise transformation.

As AI adoption in insurance matures, I expect insurers' investment priorities to gradually shift from infrastructure and technology toward operational transformation. Organizations that begin this work early will be able to realize business value from AI sooner and respond to changing customer expectations faster than competitors.

Senior Insurance IT & AI Consultant, ScienceSoft

References

- Insurance Industry Spending Billions on AI With Little to Show for It, New Research Finds from Simplifai (Simplifai, April 2, 2026).

- Insurance insights: 2026 AI Impact Survey Report (Grant Thornton, April 21, 2026).

- Insurer IT Budgets and Projects, 2026 (Datos Insights, April 7, 2026).

- Consumer Support for AI in P&C Insurance Nearly Doubles in 2026, Insurity Survey Finds (Insurity, April 21, 2026).

- Best’s Special Report: AM Best Survey Finds Most Insurers Expect to Leverage AI Though Data, Security Challenges May Impede Fast Adoption (AM Best, April 27, 2026).

- Global InsurTech Report. Artificial Intelligence — Risks and Opportunities in (Re)insurance and Beyond; Q1 — Digital Risks (Gallagher Re, May 2026).

- State Farm Details Next Gen Good Neighbor ‘Human + Digital’ Approach to Deliver Unmatched Customer Experience (State Farm, May 12, 2026).

- Liberty Mutual Insurance Launches First-of-its-Kind Carrier-Backed Conversational AI Quoting App in ChatGPT for Auto Insurance (Liberty Mutual Insurance, May 28, 2026).

- Travelers Launches AI-Powered Claims Intelligence Tool in e-CARMA® (Travelers, May 1, 2026).

- The Baldwin Group Announces Expanded Enterprise Relationship with Anthropic to Accelerate Scaled Deployment of Advanced AI Across Insurance Operations (The Baldwin Group, May 4, 2026).

- BriteCore Unveils AI Strategy for P&C Insurers, Launches First Wave of Embedded AI Copilots (BriteCore, May 20, 2026).

- Duck Creek Launches Insurance-Native Agentic AI Platform and Unveils New Applications to Transform Underwriting and Claims (Duck Creek, April 28, 2026).

- We just launched the first agentic AI underwriting platform for industrial cyber insurance. Here's why it matters (DeNexus, May 11, 2026).

- Gallagher Launches Gallagher Blueprint, Pairing AI and Expert Insight to Produce Risk Profile Scores and Market-Ready Action Plans (Gallagher, May 4, 2026).

- Marsh Risk unveils AI-powered Risk Companion suite of analytics to empower clients with faster, smarter risk management (Marsh Risk, April 28, 2026).

- Learning about new capabilities hitting our industry at Insurtech Insights in NYC (Grant Donkervoet, June 2026).

- The 93/7 Problem: Why Companies Are Spending Their AI Budgets Backward (Forbes, May 6, 2026).

- Implementation of NAIC Model Bulletin: Use of Artificial Intelligence Systems by Insurers (NAIC, June 4, 2026).