CRMs can employ large language models (LLM) to automatically capture meeting notes, transcribe calls, and summarize email and chat conversations with customers and producers. LLMs can log structured communication summaries into the customer record and vet conversations for compliance. They can be tasked to generate personalized offering emails, renewal reminders, claim status updates, and policy summaries. Users can review, edit, and approve AI-generated content before distributing it.

CRM for Insurance Companies

Features, Pragmatic Customization Paths, Costs

ScienceSoft engineers tailored insurance CRM solutions and components that address the structural gaps of off-the-shelf CRMs, such as rigid automation and compliance logic, predefined integrations, and fragmented customer data. Our clients get interoperable CRM systems that can quickly adapt to evolving products, distribution channels, claims workflows, and regulatory rules while ensuring predictable TCO.

Contributors

Vital Soupel

Senior Insurance IT & AI Consultant, ScienceSoft

Olga Vinichuk

Insurance IT & AI Consultant and Lead Business Analyst, ScienceSoft

Insurance CRM at a Glance

Insurance customer relationship management (CRM) software is necessary to manage omnichannel interactions with insurance customers and coordinate servicing activities across sales, policies, and claims. It consolidates customer data and automates onboarding, documentation, and marketing workflows.

- Key integrations for an insurance CRM platform: a policy administration system, claim management software, distribution platforms, communication channels, and more.

- Implementation time: around 7–15 months for the first release of custom CRM (core software modules).

- Development costs: from $20,000 for small CRM components to $1,000,000+ for large-scale platforms. Use our free calculator to estimate the cost for your case.

Insurers’ demand for deeper CRM customization is growing

Many of ScienceSoft’s insurance clients who use generic CRMs like Microsoft Dynamics 365 or HubSpot admit that the standard functionality limits how much they can scale horizontally. Even those who rely on niche tools like Salesforce for Insurance often struggle with setting up specific engagement models, non-standard integrations, and regional compliance rules. Since insurers increasingly want to use AI trained on their internal knowledge, integration gaps and the resulting data silos in off-the-shelf CRM suites become even more frustrating.

It doesn’t mean you have to invest in developing a fully custom CRM. In most situations, the most feasible path is taking an existing CRM platform and adding the missing features, business logic, data layers, and custom integrations. The result is a CRM that still feels familiar but adapts to the way you want to work, and not the other way around. The depth of customization will be dictated by the complexity of your insurance products, distribution networks, and core stack: the weirder the needs, the more custom code you’ll have to add.

Where Tailored Insurance CRMs Outshine Off-the-Shelf Suites

|

|

Support for diverse insurance products, including specialty and alternative plans, and complex distribution models, including tiered brokerage and embedded insurance partnerships. |

|

|

Integration with any necessary software, including legacy policy administration and claim tools, local customer data platforms and distribution networks, and modern insurtech services. |

|

|

|

|

|

Data orchestration across multiple CRM-focused data platforms and task-specific tools, allowing insurers to unify data models and digital workflows and leverage straight-through automation at scale. |

|

|

Ability to quickly tweak and extend the CRM with new custom features when new business rules, insurance products, distribution models, or regulatory requirements emerge. |

|

|

Support for proprietary AI models and custom agentic components with full control over AI setup, allowing continuous fine-tuning of technical guardrails and governance models to ensure accurate and compliant AI behavior. |

ROI for Insurance CRM Solutions

Based on case studies by leading agencies such as Forrester and Nucleus Research, market-leading CRM software suites can deliver an ROI of 125–500%, with a typical payback period of 6–7 months. Nucleus Research also reports that the median return on packaged CRMs has seen a steady decline over the past decade, mainly due to slow product adaptation to the increasingly complex technology landscape.

Consultants at ScienceSoft estimate that tailored insurance CRM systems, due to their greater agility and adaptability, can deliver, on average, 1.5x the payoff of off-the-shelf tools.

Here are the operational and financial outcomes reported by the insurance market players who adopted customized CRMs:

40%+higher productivity of insurance agent teams due to CRM workflow automation and improved visibility of customer interaction tasks. Source: Damco. |

30–40%+quicker customer onboarding and response to claims and servicing inquiries due to unified, automated CRM workflows. Source: MapleSage. |

Up to 10%growth in revenue driven by higher capacity of relationship managers and more effective insurance cross- and upselling. Source: Salesforce. |

Insurance Firms That Can Benefit From Tailored CRM Software

Third-party administrators (TPAs)

Distribution facilitators (NMOs, banks, embedded insurance providers)

Functionality of Customized Insurance CRM

Below, ScienceSoft’s consultants list the core building blocks that insurers often need in their CRM solutions. We can implement any combination of them as a standalone system or build a custom module or workflow on top of your existing CRM suite:

![]()

Insurance sales management

CRMs can support direct sales, brokers, agents, and embedded insurance partners with separate workflows and KPIs for each distribution channel. Using a no-code process design engine, staff can set up channel-specific rules, targets, and KPIs, compare actual and planned results by product, region, and producer, and collaborate on pipeline plans around shared accounts or opportunities. ScienceSoft can develop insurance CRM software to help manage customer relationships and sales pipelines.

![]()

Lead and opportunity management

Leads from websites, partner portals, and other channels flow into one pipeline. The CRM captures submission details, follows up on missing information, scores opportunities against preselected criteria, and routes each case to the right agent, underwriter, or product specialist. Users can monitor leads and opportunities by line of business in dynamic dashboards.

![]()

KYC checks and sanctions screening

CRM engines can automatically extract customer data from digital submissions and handle KYC checks in compliance with the insurer’s internal guidelines and region-specific regulatory rules. They validate customer data against trusted third-party sources (government registries, OFAC databases, credit bureaus, etc.), flag discrepancies and high-risk cases, and route them for manual review, logging all KYC steps and outcomes for audits.

![]()

Customer profiling

CRMs can automate template-based profiling of individual, commercial, and group insureds, populating template forms with information on customers, insured objects, and risk attributes. For group and commercial coverages, the CRM can structure parties according to user-defined household, parent-subsidiary, branch, and affiliate hierarchies. Users can also apply custom criteria for customer clustering, e.g., by product line, jurisdiction, or risk class.

![]()

Quote and document generation

Users can create tailored templates for insurance documents (quotes, invoices, COIs, renewal offers, and more). When triggered to generate a document, CRMs choose the right template form and insert customer and policy details based on preset rules. They can route document drafts for review to underwriters, legal teams, or managers and automatically distribute approved documents internally and across specific interaction channels.

![]()

Policy lifecycle servicing

CRMs continuously aggregate data on active policies and policy lifecycle events (quotation, endorsements, renewals, etc.). They monitor upcoming policy expirations, identify lapse risks, and trigger renewal notifications and pre-renewal workflows for policyholders, brokers, and internal teams. A customized CRM can automate the capturing of omnichannel customer requests for policy changes and inquiry processing according to firm-specific SLAs.

![]()

Claim and settlement tracking

Teams can track new claims, milestones, and real-time claim processing statuses within the policyholder records in CRM. The system captures new claims, links them to the relevant customer profiles, and records information on third-party vendors involved in claim handling. Configurable notifications inform teams about claim status changes, pending documents, reserve updates, and settlement approvals.

![]()

Omnichannel customer communication

CRM platforms provide a collaborative space for planning and tracking insurance customer communication. Users can create tailored message templates and call scripts for various cases. The CRM distributes customer messages and triggers IVR-driven automated calls. It can apply natural language processing (NLP) technology to interpret textual customer responses and transcribe voice inputs.

![]()

Marketing automation

Marketing teams can plan segment-specific and personalized customer offers, run campaign scenario modeling, and calculate performance impact metrics. CRMs can automatically launch marketing campaigns based on policyholder interaction events, policy milestones, coverage gaps, or risk profile changes. They support rule-based policy bundling and rider adding for cross-sell and upsell campaigns.

![]()

Customer experience management

CRMs let insurers model end-to-end customer journeys across sales, onboarding, servicing, and claims and analyze CX friction points. The solution captures customer service requests, triggers and tracks resolution workflows, and calculates CX metrics. It can also launch customer feedback surveys after key interactions (e.g., policy issuance, claim) and automatically process responses.

![]()

CRM platforms can calculate, track, and report any selected metrics across sales, customer service, CX, marketing, and finance. They can accommodate standard KPI formulas and proprietary models for company-specific indicators. Predictive analytics engines can model and forecast demand, renewals, churn, cross-sell propensity, SLA adherence, and CLV. Customizable dashboards display metrics at the customer, segment, and portfolio levels.

![]()

Producer relationship management

CRMs can automatically process producer documents, verify licensing and compliance status, and create structured partner profiles. Carriers can configure tailored commission models by product, premium band, and producer performance tier and monitor partner-level written premiums, bind ratios, policy sizes, loss ratios, and retention rates. CRM engines automatically calculate commissions and trigger payouts based on predefined events.

![]()

Operational compliance

CRMs monitor employee compliance with internal customer servicing and communication guidelines. They can verify adherence to the company-relevant regulatory frameworks (e.g., KYC/FinCEN, UTPA, TCPA, the NAIC case handling and timeline rules for the US insurers) and data protection standards (the NAIC Insurance Data Security Model Law, HIPAA, GLBA, CCPA/CPRA, NYDFS, GDPR, DORA, etc.).

![]()

Data security

CRM systems maintain a complete log of user activities and customer interactions. CRM admins can define granular permissions for users to access and manipulate specific data (by role, product line, region, and more). The system automates role-based access control, encrypts and tokenizes data for storage and transfer, and deletes data according to preset retention and deletion policies.

Why CRM and third-party portals deserve separate tracks

Many CRM vendors market customer and producer portals as modules within a CRM suite. In reality, portals are standalone tools with different user journeys, logic, security approaches, scalability needs, and often even different tech stacks. Moreover, ScienceSoft’s experience shows insurers rarely require the same depth of customization in a CRM as they do in external portals. Most often, our clients choose to customize a CRM product for internal teams and build fully custom apps for third-party self-service. This gives them tighter control over data exposure, process design, and how security and performance are handled.

One lesson we’ve learned from complex digital transformation initiatives is that running CRM and portal development as parallel but separate projects often delivers better results. It allows teams to move faster in requirements engineering, keep scope and budgets sharper, minimize architectural trade-offs, and speed up go-live for both solutions.

How AI Can Reinforce Insurance Customer Relationship Management

Insurers are increasingly deploying artificial intelligence in their service operations, with 86% of domain players planning to increase AI investments in 2026. According to McKinsey, AI-powered automation of customer interaction planning, message delivery, lead generation, and cross-selling can help reduce customer service costs by 20–30%, grow revenue by 5–8%, improve customer satisfaction rates by 15–20%, and cut churn by up to 60%.

ScienceSoft suggests extending your insurance client management software with the following AI features for comparable gains:

GenAI-powered communication processing and drafting

AI-driven predictive analytics for sales and marketing

Tailored machine learning (ML) models can be applied to score leads, rank opportunities, and prioritize high-value prospects. Predictive ML algorithms can also analyze retention patterns, cross-sell history, and loss history and forecast customer lifetime premium value and renewal likelihood. They can spot policyholders with high non-renewal risk and trigger targeted retention workflows. Marketing teams can use ML-produced insights to define campaign audiences and optimize budget allocation.

Intelligent document processing

Image analysis and LLM technologies empower CRMs to retrieve structured data from multi-format submissions (ACORD, EDI, custom forms, etc.) and supporting documents and map the extracts to predefined CRM fields. Intelligent algorithms can validate the submitted documents for accuracy, completeness, and authenticity and recognize nuanced alterations that static algorithms can struggle with, including document changing and faking using generative AI.

AI-supported sentiment analysis

CRMs can use LLMs or NLP engines to analyze customer communications and CX feedback, identify explicit and implicit dissatisfaction signals related to premium increases, claim delays, denied coverage, or service complaints, and flag churn-prone customers for outreach. They can track sentiment trends, highlight recurring issues, and feed the insights into renewal and retention models to refine churn prediction and outreach timing.

AI-assisted data search and service personalization

Employees can ask generative AI assistants to retrieve customer information from data repositories, check policy, billing, renewal, and claim statuses, and suggest the optimal forms, timings, and channels for personalized communications. Smart copilots can suggest cross-sell, upsell, renewal, and retention outreach and craft optimal product bundles, riders, and coverage limit adjustments. Customer assistants can aid insureds in data search, product selection, and problem-solving.

Agentic automation of multi-step CRM workflows

AI agents can orchestrate and execute predefined customer relationship workflows with minimal manual coordination. For example, in the claim intake process, agents can capture claims, run call-based loss validation, trigger and track adjustment workflows, draft claim status messages, and send them to customers. In customized CRMs, insurers can control the degree of agent autonomy via tailored authorization rules and human approvals for complex and exception cases.

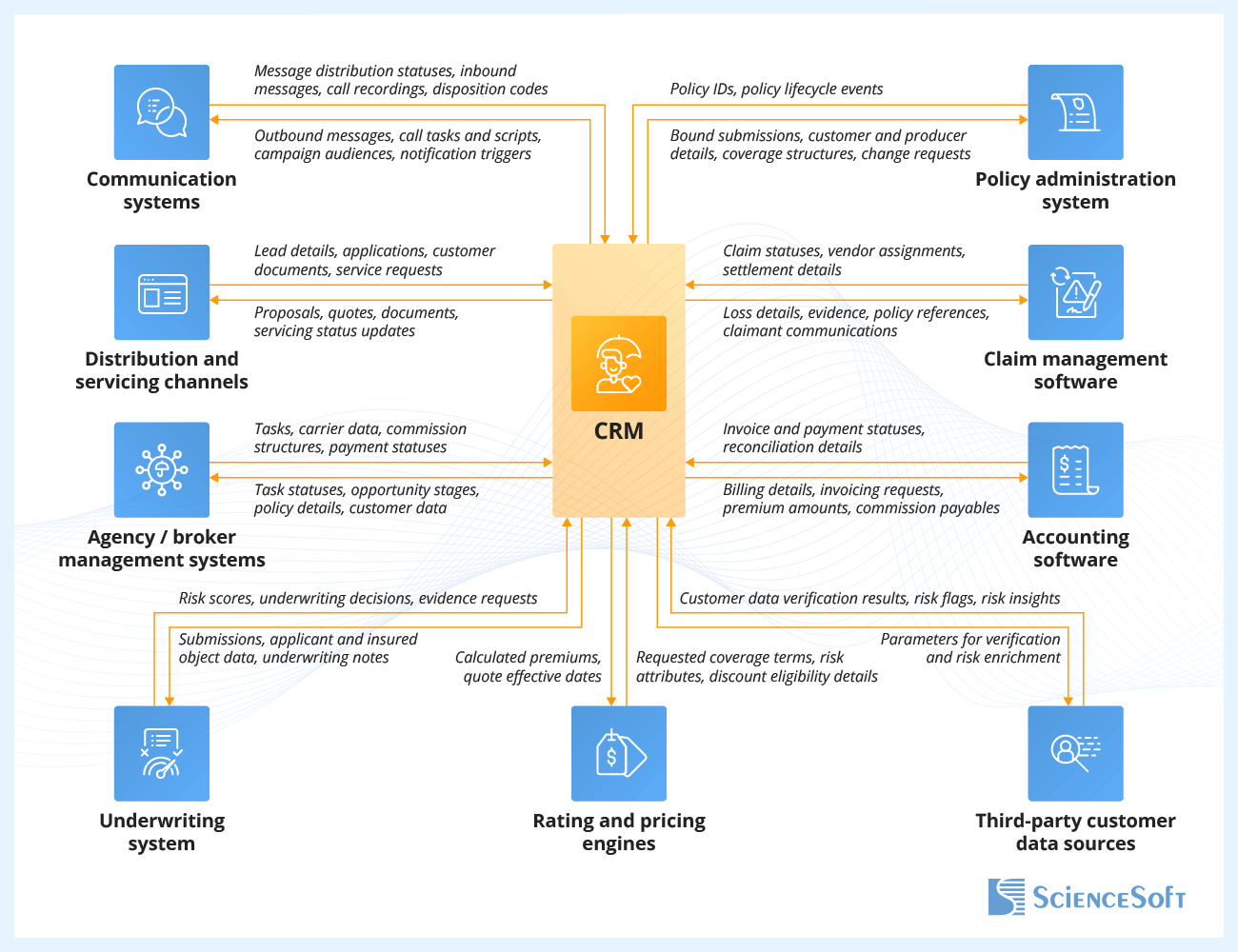

Essential Integrations for Insurance CRM Platforms

Distribution and servicing channels

To route submissions to underwriters, streamline underwriting progress tracking for front-line teams, and coordinate evidence collection and decision communication.

Rating and pricing engines

To generate personalized quotes in line with the insurer’s current rates and pricing logic and streamline premium recalculation after customer and policy data changes.

To speed up policy issuance and customer-requested policy adjustments, track current policy statuses, and trigger policy renewal and servicing workflows.

To quickly pass claims to adjusters and plan claim-related policyholder interactions.

To auto-populate invoices with customer data, trigger billing reminders, initiate interactions for delinquent accounts, and share details on producer commission payments.

NB: If you run billing and payments and general ledger accounting in different systems, your CRM will require integration with both.

Third-party customer data sources

ID and business registries, AML/OFAC databases, credit and fraud databases, risk data platforms (e.g., LexisNexis, Verisk), etc.

To automatically validate the data provided by customers and enrich submissions with third-party risk and eligibility insights during onboarding and servicing.

Communication systems

E.g., email, SMS, and messaging platforms, call center/CTI systems, IVR systems.

To orchestrate customer interactions across channels, automate personalized reminders and alerts, and run targeted digital marketing campaigns.

For insurance agency CRM and insurance broker CRM

To sync data on sales and servicing activities with the producer’s system of record, streamline coordination of prospecting, renewal, and servicing workflows, and reconcile commissions.

How to Customize Your Insurance CRM Solution

|

|

Platform-based development |

Engineering from scratch |

|---|---|---|

|

Best for

|

Insurance organizations that already have a CRM foundation (a specialized or enterprise suite) and only need small-scale, tailored automation modules or an orchestration layer for scattered workflows. |

Insurers with large-scale or unique CRM operations that require highly specific automation features, need unified CRM workflows across multiple jurisdictions, or are transitioning from legacy, home-grown CRM suites. |

|

Pros

|

|

|

|

Cons

|

|

|

|

Tech stack we use

|

|

|

Best Practices for Insurance CRM Development

Below, ScienceSoft’s consultants share best practices to create reliable CRM for insurance companies while reducing development costs and timelines. These apply regardless of your chosen development approach.

![]()

Architecting CRM as part of a broader IT system helps optimize TCO

Looking at the broader software ecosystem rather than the CRM capabilities alone helps determine which digital workflows can be more sustainably and cost-effectively handled by external systems.

In one of ScienceSoft’s health insurance CRM projects, the client initially planned to store all documents directly in Dynamics 365 Sales. However, the anticipated high volume of documents would have quickly led to storage shortages and rising licensing costs. By looking at the insurer’s broader IT ecosystem at the early design stage, our architects identified that a dedicated document management system integrated with the CRM would handle customer document automation more efficiently than the CRM platform. This architectural decision improved long-term CRM scalability, preserved system performance, and optimized TCO.

![]()

Reusing components and services from CRM vendors cuts the cost of custom development

Many leading CRM platforms offer robust sets of prebuilt UI components, APIs, middleware services, SDKs, and low-code extension mechanisms that can significantly reduce development effort and architectural complexity when extending an existing CRM system for insurance with custom modules.

For example, Microsoft’s ecosystem around Dynamics 365 Sales includes reusable UI and back-end building blocks, Dataverse as a structured data layer, the Power Platform for building and packaging custom logic (Power Apps, Power Automate), and well-documented APIs and event-driven integration surfaces that support custom modules and external services. Leveraging these vendor-native capabilities minimizes the share of costly custom coding, reduces integration risks, and ensures alignment with future product updates. It also enables custom extensions to inherit the platform’s security model, compliance controls, and QA processes without additional overhead.

![]()

CRM data should be prepared before launching AI extensions

Fragmented, inconsistent, and poorly governed data remains one of insurers’ most persistent challenges. And you can’t introduce AI into insurance CRM workflows reliably and safely without refining data models and integration infrastructure.

To prepare your data for AI, you usually need to implement canonical insurance data models, establish unified customer and policy identifiers, enforce clear system-of-record boundaries, introduce data quality controls, and ensure metadata, lineage, and access governance. ScienceSoft’s data engineers streamline this groundwork through API-first and event-driven integrations, structured ELT/ETL frameworks, automated data validation pipelines, MDM-driven identity resolution, and governed analytical storage (such as a data warehouse or a lakehouse) that provide AI models with consistent, traceable historical insurance data.

Costs of Insurance CRM Solutions

Building insurance customer relationship management software may cost from $20,000 to $1,000,000+, depending on the solution’s functional scope, the number and complexity of integrations, non-functional (performance, scalability, security, compliance) requirements, and the chosen development path.

Sample cost ranges

Here are ScienceSoft’s estimates for CRM solutions commonly requested by our insurance clients:

![]()

$20,000–$50,000

We implement a commercial CRM (e.g., Microsoft Dynamics 365 Sales, Microsoft Dynamics 365 Customer Service, Salesforce for Insurance) and customize it to your customer relationship management processes through prebuilt plugins and extensions. The platform supports operations across 1–3 traditional insurance lines in a single jurisdiction (e.g., US, KSA).

![]()

$50,000–$300,000+

We use a market-available CRM suite as a foundation and add custom features and integrations to align it with your workflow needs and IT environment. Custom modules automate specific CRM workflows (e.g., customer interaction, marketing, compliance controls) using rule-based engines, with possible extensions to advanced analytics and AI assists.

![]()

$100,000–$400,000

We build a CRM data consolidation layer that aggregates data in batches from 3–15 sources (distribution platforms, PAS, claims system, KYC databases, interaction tools, etc.). It automatically processes structured and semi-structured data, maps all data into a unified format, and prepares it for analytics and data-driven automation. The solution comprises a data warehouse and can include BI capabilities.

![]()

$400,000–$1,000,000+

We engineer a custom CRM system for your unique processes. The solution automates customer profiling, policy and claim servicing, marketing, and risk management operations using low-code workflows, custom rules, and, if needed, tailored AI components. It supports the necessary insurance products, distribution models, jurisdictions, and integrations with corporate and external systems.

* The final implementation cost will depend on the maturity of the company’s IT ecosystem and the complexity of data migration procedures.

Learn the Cost of Your Tailored Insurance CRM Solution

Please answer a few simple questions prepared by ScienceSoft's consultants — within 24 hours, our team will carefully review your project details and calculate a free custom quote.

Discover our insurance software development services in detail.

1

1.1

1.2

2

3

4

5

6

7

8

9

Thank you for your request!

We will analyze your case and get back to you within a business day to share a ballpark estimate.

In the meantime, would you like to learn more about ScienceSoft?

- Project success no matter what: learn how we make good on our mission.

- Since 2012 in insurance IT services: check what we do.

- 4,300+ successful projects: explore our portfolio.

- 1,500+ incredible clients: read what they say.

Why Develop Insurance CRM Software With ScienceSoft

-

Since 2012 in engineering custom software solutions for the insurance industry.

- Since 2008 in full-cycle CRM consulting and development.

- Insurance IT and compliance consultants (NAIC, HIPAA, NYDFS, GDPR, etc.) with 5–20 years of experience.

- 45+ certified project managers (PMP, PSM I, PSPO I, ICP-APM) who succeeded in large-scale projects for Fortune 500 firms.

- 30+ architects with hands-on experience in designing complex insurance systems and driving secure implementation of emerging technologies.

- 350+ software engineers, 50% of whom are seniors or leads.

- Established practices to ensure the high quality of insurance solutions and their delivery on the agreed timelines and budget, despite project constraints or uncertain requirements.

ScienceSoft’s approach, as seen through our clients’ eyes

ScienceSoft are responsive, technically sharp, and they communicate well with our people. When we've needed to move fast, they've stepped up and delivered. What I appreciate most is their proactive approach. They don't just wait for us to identify issues. They bring solutions to the table and help us prioritize what matters most. That kind of partnership is hard to find.

ScienceSoft demonstrated a deep understanding of our requirements, and their insurtech developers needed minimal supervision.

What stood out was ScienceSoft's proactive suggestions for cost-saving architecture design and tech stack solutions. Their input ensured we stayed within budget without compromising on software quality. The value we derived from partnering with ScienceSoft is definitely worth the investment.

Partnering with ScienceSoft has been an excellent experience. Their team transformed our underwriting platform into a well-oiled machine. They identified and fixed several longstanding issues that had been causing us persistent difficulties. Their communication was exemplary; unlike our previous experiences with outsourcing, we never had to chase them for updates, and they were always prompt in responding to our queries.