Insurance Billing and Payments Software

Features, Development Best Practices, Costs

ScienceSoft engineers custom insurance billing and payment solutions that address the common drawbacks of off-the-shelf tools, such as constrained billing and payout models, predefined integrations, and limited support for local regulations. Our clients get secure, interoperable solutions that can quickly adapt to change while ensuring predictable TCO.

Insurance Billing and Payments Software at a Glance

Insurance billing and payment software automates premium billing, payment collection, commission payouts, and claim disbursements across insurance products. It can provide a unified view of billing accounts, payment obligations, and related transactions and include payment risk management features.

- Key integrations for an insurance billing and payment platform: a policy administration system, claim management software, insurance portals, payment utilities, and more.

- Implementation time: around 7–15 months for the first release (core software modules).

- Development costs: from $100,000 for a focused process improvement module to $1,500,000+ for a large-scale custom billing and payments system. Use our free calculator to estimate the cost for your case.

Why Insurers Opt for Custom Billing and Payment Software

When off-the-shelf billing or payment tools cannot fully support the insurance firm’s product logic, partner arrangements, legacy integrations, or servicing workflows, insurers typically choose one or several of these custom implementation paths:

- Build a focused custom module to fix the costliest operational bottlenecks first. This approach lets insurers automate specific billing and payment tasks without changing core systems and compromising logic customization. Custom modules also work well to accommodate non-standard billing and payout models, such as dynamic billing for pay-as-you-live health programs or risk-based payouts for parametric insurance.

- Launch a targeted self-service or process optimization solution to improve customer and partner experiences and enhance the efficiency of current billing and payment workflows. Insurers often take this path to introduce customer and producer portals and leverage tailored finance automation features powered by generative and agentic artificial intelligence (AI).

- Add a billing and payment orchestration layer that standardizes workflows, business rules, and exception handling across insurance systems, servicing channels, and jurisdictions. Custom setups can support proprietary orchestration rules and operational regulations relevant to the firm’s activity, including local frameworks and plan-specific mandates.

- Develop integrations and a shared financial data flow so billing events, payment statuses, commissions, and disbursements stay consistent across the insurer’s, partner, and customer-facing systems. Custom integration layers allow applying tailored data architectures and connecting any necessary software, including legacy carrier systems, niche distribution platforms, and local payment utilities.

- Build customizable API interfaces so partners (agencies, MGAs, TPAs, etc.) can embed automation features from the carrier’s insurance invoicing software and payment apps in their own apps. This is a common path for insurers with large partner networks and companies seeking to productize their home-grown insurance billing and payment suites.

- Engineer a full-scale custom billing and payments solution when product diversity and complexity, proprietary distribution models, tiered partner arrangements, multi-entity operations, legacy system constraints, or regional requirements make off-the-shelf tools too rigid or too expensive to adapt.

Major ROI Drivers for Insurance Billing and Payment Solutions

The returns for insurance billing software and payment solutions are driven by improved operational efficiency, enhanced employee capacity, and minimized manual errors achieved through a high degree of workflow automation.

Based on ScienceSoft’s proprietary research and previous projects, tailored tools can help insurers hit the following automation benchmarks:

Sources: The Hackett Group, KPMG, SAP Fioneer, HighRadius, Billtrust.

Functionality of Insurance Billing and Payment Software

Below, ScienceSoft’s consultants list the features that lay the foundation for a robust insurance billing and payment system. We can add these functions to your existing insurance platforms, build a module or a standalone solution for a specific task area, or develop full-featured software for end-to-end billing and payment automation.

![]()

Billing plan management

- Setting up and configuring custom parameters for insurance billing plans (by policy type, program, customer segment, jurisdiction, etc.):

- Billing models: one-time, installments, deposit and audit (e.g., for workers’ compensation plans), pay-as-you-go, etc.

- Installment billing schedules: monthly, quarterly, semi-annual, etc.

- Premium financing terms (installment APR, per-payment fees).

- Payment modes: card, bank transfer or ACH, digital wallet, e-check, payroll deduction, etc.

- Payment due dates and grace periods.

- Payment-driven policy reinstatement and cancellation rules, including reinstatement windows and short-rate/pro-rata return premium handling logic.

- Tailored multi-party billing plans, e.g., parent entity plus subsidiaries on one coverage, employer and employee plans with contribution splits, and co-insurance splits.

- Auto-applying the preset billing terms to product-specific billing plans.

![]()

Premium billing

- Automated aggregation of data on due premium payments from connected distribution, servicing, and policy administration systems.

- Calculating premiums, jurisdiction-specific taxes, discounts, additional charges (e.g., surplus lines fees, installment fees), and contribution breakdowns (for group policies) to cover in the invoice based on the insurer’s proprietary formulas.

- Creating custom invoice templates tailored to insurance line, program, jurisdiction, currency, language, etc.

- Automated generation of one-time and recurring customer invoices.

- Automated generation and insertion of unique QR codes and payment links in the invoices.

- Automated invoice validation based on preset SLA and billing guidelines.

- Multi-party approval workflows for complex invoices (e.g., for layered or scheduled commercial coverage).

- Scheduled and ad hoc invoice sending to customers via digital channels.

- (For customers) Insurance portals and self-service apps to manage billing details, view due invoices and payment history, pay premiums by a preferred payment method, and track payment status.

- (For the KSA) Applying region-specific e-invoice elements, such as a unique QR code for e-invoice data validation.

![]()

Premium payment processing

- Automated processing of multi-currency premium payments via a custom payment gateway or third-party payment gateways (of banks or independent payment providers, e.g., PayPal, Stripe).

- Automated payment collection by direct debit, with the policyholder’s prior consent.

- Recording full and partial down payments and installment payments against outstanding invoices, including suspended posting until remittance is complete.

- Automated customer notification and payment retry in case of payment failure based on preset retry rules (e.g., retry cadence by method, gateway auto-switching, expired card handling).

- Automated allocation of received payments across insurer accounts, with rule-based amount splits across premium trust and operating accounts, entity-specific accounts, product-specific accounts, etc.

- Automated processing of refunds and chargebacks to the customer’s original payment method.

![]()

Delinquency management

- Continuous analysis of due and received customer payments and automated spotting of delinquencies.

- Prioritizing collection activities based on debt aging, debt amount, policyholder value and risk, and more.

- Automated scheduling and assignment of collection tasks.

- Template-based creation of textual reminders on due payments for various policyholder segments, tailored by language, frequency, tone, etc.

- Scheduled distribution of textual and voice payment reminders to insurance customers (via email, SMS, a customer portal, in-portal chatbots, and more).

- Automated collection calls using IVR bots.

- Automatically capturing and processing policyholder responses and promises to pay, including those in textual format and in the form of recorded voice messages.

- Instant routing of customer responses that cannot be automatically processed to manual handling.

- Automated enforcement of policy termination upon insurer-defined events (e.g., a customer’s refusal to pay, non-payment for a specific period).

- A centralized dashboard with an overview of delinquent payments and collection-related customer interactions.

![]()

Commission management

- Configuring carrier-specific commission logic (by agent tier, insurance line, policy type, etc.):

- Commission amounts: percentage of written premium, flat per-policy fee, tiered rate by volume, etc.

- Commission bases (written, collected, or earned premium) and required evidence (e.g., installment receipts, monthly reports).

- Overrides and bonuses: new business, persistency, etc.

- Chargeback and clawback rules for policy changes.

- Automated calculation of agent-level and agency commissions based on the current policy and premium data.

- Scheduled and ad hoc commission payouts, including automated disbursements via direct deposit.

- Auto-correction of agent commissions based on premium updates, cancellations, refunds, etc.

- Automated generation of commission reports and tax documents (e.g., 1099/PPY, W-2).

- (For agents) Self-service agent portals to track historical earnings, pending commissions, reports, and tax documents.

![]()

Claim payment management

- Automated initiation of claim payouts based on:

- Requests for full or partial policyholder reimbursement submitted by adjusters.

- New service invoices submitted by claim execution partners (repair vendors, restoration firms, legal counsels, etc.).

- (For parametric plans) Predefined risk escalation events.

- Automated processing of partner invoices.

- Automated calculation of due payout amounts for partial claim payments, including complex schemes like property ACV payments followed by RCV holdback releases or double-trigger parametric payouts.

- Rule-based assignment of optimal bank accounts and payment methods for claim payouts.

- A customizable claim payment calendar with cut-off times and mass-payment runs.

- Scheduled and ad hoc enforcement of domestic and cross-border claim payments across settlement utilities.

- Rule-based, straight-through payouts for simple claims.

- Multi-party payment authorization for large and complex claims.

- Automated calculation of reinsured claim share values and cash call submission to reinsurance partners.

- Reinsurer payout progress tracking.

![]()

Payment control and reconciliation

- Real-time payment tracking by status: approved, invoice sent, paid, partially paid, overdue, etc.

- Configurable payment control dashboards for various user roles: billing specialists, accounts payable specialists, loss adjusters, payment analysts, and more.

- Automatically matching data on payment transactions with the data provided in bank statements.

- One-to-one, one-to-many, and many-to-many (e.g., bulk agency remittances across many policies) transaction reconciliation based on the insurer-defined rules.

- Automatically defining payment discrepancies (e.g., duplicate postings, mismatched invoice IDs, short pays) and marking them to be reconciled manually.

- Rule-based posting of reconciled transactions to the insurer’s accounting ledgers.

- Monitoring billing and payment compliance with the insurer’s internal policies and operational regulations, such as the NAIC Prompt Payment of Claims Model Act, state DOI regulations, CMS billing and premium collection rules for Medicare Advantage and Part D plans, and TRIA/TRIP surcharge handling requirements for the US insurers.

- Notifications on the sent and received payments, payment delays, transactions requiring manual handling, and more.

![]()

- Automated detection of general and insurance-specific payment fraud schemes, including:

- Duplicated billing, invoice inflation, upcoding (in health insurance).

- Customer and agent premium diversion.

- Fee churning.

- Last-minute payment instruction manipulations.

- Refund abuse.

- Employee and customer account takeovers.

- Fraud risk scoring based on the insurer’s custom formulas.

- Monitoring payment activities and analyzing their compliance with the preset workflow standards.

- Flagging employee non-compliance cases (missing payment approvals, unauthorized editing of payment details, etc.).

- Instant notifications about suspicious transactions to payment risk investigation teams and SIUs.

- Automated risk response enforcement, e.g., blocking payments until review or triggering transaction hard-stops if a case is proven fraudulent.

- Configurable workspace for investigators to manage payment fraud and non-compliance cases.

- Automated generation of fraud reports, including suspicious activity reports (SARs) and suspicious transaction reports (STRs).

- Rule-based submission of approved fraud reports to regulatory entities (e.g., state insurance departments, FIUs, NICB for the US) and business partners (e.g., reinsurers).

![]()

- Calculating and tracking essential financial metrics: total written and collected premium, outstanding A/R, claim payouts, commission payable, DSO, DPO, A/R and A/P turnover, reinstatement rate after non-pay cancellation, and more.

- Automated detection of areas of poor and superior performance, e.g., insurance products with high delinquency rates, agencies with slower remittance, states with longer claim payout cycles.

- Analytical dashboards with an aggregated view of insurance payment KPIs with slice-and-dice options for multidimensional data visualization.

- Automated generation of billing and payment reports for operational teams, partners, and regulators.

- Trend-based forecasting of cash flow amounts and dates (by line, program, jurisdiction, branch, customer segment, etc.).

- Scenario modeling for policy lifecycle events (e.g., lift in renewals, premium rate increase, commission shrinkage) and automated evaluation of their impact on cash flows.

![]()

Payment data security

- Payment data encryption in transit and at rest.

- Data masking and tokenization for sensitive payment attributes (e.g., PAN and bank account numbers).

- Permission-based access to insurance payment data.

- Multi-factor user authentication.

- End-to-end audit trail for payment-related activities.

- Digital signature workflows for payment documents.

- Support for compliance with global, region- and industry-specific payment data protection standards and regulations, including the NAIC Insurance Data Security Model Laws adopted at the state level, GLBA, NYDFS, HIPAA (for the US health insurance), SOX, SOC1 and SOC2, GDPR (for the EU), ZATCA (for Saudi Arabia), PCI DSS (for insurers retaining payment card data), and more.

- Automated payment data deletion according to preset retention and deletion policies.

- (For the KSA) Invoice data hashing and timestamping.

How AI Can Reinforce Insurance Billing and Payments

47% of insurers report already having live artificial intelligence solutions running across the organization and delivering business value. Generative and agentic AI are increasingly gaining traction as the next big value drivers: in claim payments specifically, early adopters have reported 95% auto-payout rates and 70% of disbursements completed within 12 hours after FNOL.

ScienceSoft’s consultants suggest that the following AI-supported capabilities can drive the highest ROI uplift for insurance billing management software and payment solutions:

![]()

Payment data validation

- Data retrieval from multi-format vendor invoices using intelligent image analysis technology.

- Invoice data validation against approved estimates, service dates, utilization limits, network prices, and more using machine learning (ML).

- Inaccuracy flagging in customer invoices (incorrect policy references, tax locations, roundings, and more), including gap spotting for complex scenarios like overlapping coverages and multi-location commercial policies.

- Payment reconciliation, discrepancy detection, and explainable suggestions on probable matches for outstanding records and transactions with incomplete references.

- AI agents for chat- and call-based verification of payment-related information provided by customers, agents, and partners.

![]()

Payment risk management

- Anomaly detection across premium, claim, and commission payment flows and dynamic risk scoring based on multiple disparate risk factors.

- Large language models (LLMs) to detect vendor invoice fraud, including subtle wording changes to justify upcoding, duplicate line items under different descriptions, and advanced forgery schemes like faked invoice imaging produced by generative AI.

- Data-driven prediction of lapse and delinquency risks and suggestions on mitigation steps (e.g., customer outreach, installment schedule tweaks).

- Intelligent detection of complex employee non-compliance cases, including coordinated approval bypasses and repeated emergency justification for specific vendors.

![]()

Billing and payment optimization

- Suggestions to insurers on optimal payment channels and timings based on channel-specific transaction costs, settlement speed, FX exposures, and case-specific priorities (e.g., settlement urgency for catastrophic claims).

- Suggestions on best retry timings and methods for failed payments.

- Data-driven suggestions on optimal claim payout amounts based on available reserves, policy limits, depreciation rules, and prior claim payments.

- AI-supported analysis of billing plan performance (remittance timing patterns, short-pay frequency, payment method costs, and more) and plan optimization suggestions.

![]()

Employee and customer assistance

- Generative AI assistants for billing and collection teams to handle payment-related data search, collection planning, and customer communication drafting and summarization.

- Payout assistants to help A/P teams and adjusters process payment documents, plan payment execution, and verify transaction compliance before disbursement.

- AI customer support agents to help policyholders understand insurance payment concepts, pay bills, and solve transactional issues.

- AI assistants for agents to interpret commission calculations, non-pay cancellations, and reinstatement conditions.

Agentic AI works best for orchestration — with strict guardrails

Some of my insurance clients worry that an AI agent could go rogue and start moving money on its own. That risk exists only in poorly designed setups. In mature ones, strong built-in controls limit everything AI can do, locking it into predictable, controlled action paths.

Guardrails are everything. We implement AI authority restriction rules to prevent agents from overriding payment instructions or triggering unintended transactions. High-risk actions like large payouts or reinstatements should always include human-in-the-loop checkpoints. You also need monitoring tools to detect AI agent behavior drifts, plus explainability and traceability tools to log every AI decision and action for internal and regulatory audits.

One more necessary limitation: agents shouldn’t touch core financial logic. Premium calculations remain inside rule-based engines, and payment execution stays with trusted integrations or RPA. Agents do what they do best: orchestrate end-to-end workflows — capture events, define automation paths, determine next steps, and trigger the right systems.

Finally, no single agent should own the entire process. ScienceSoft’s default practice is to segregate agentic duties so each agent operates within narrow, task-specific permissions. This removes single points of failure in end-to-end automation systems.

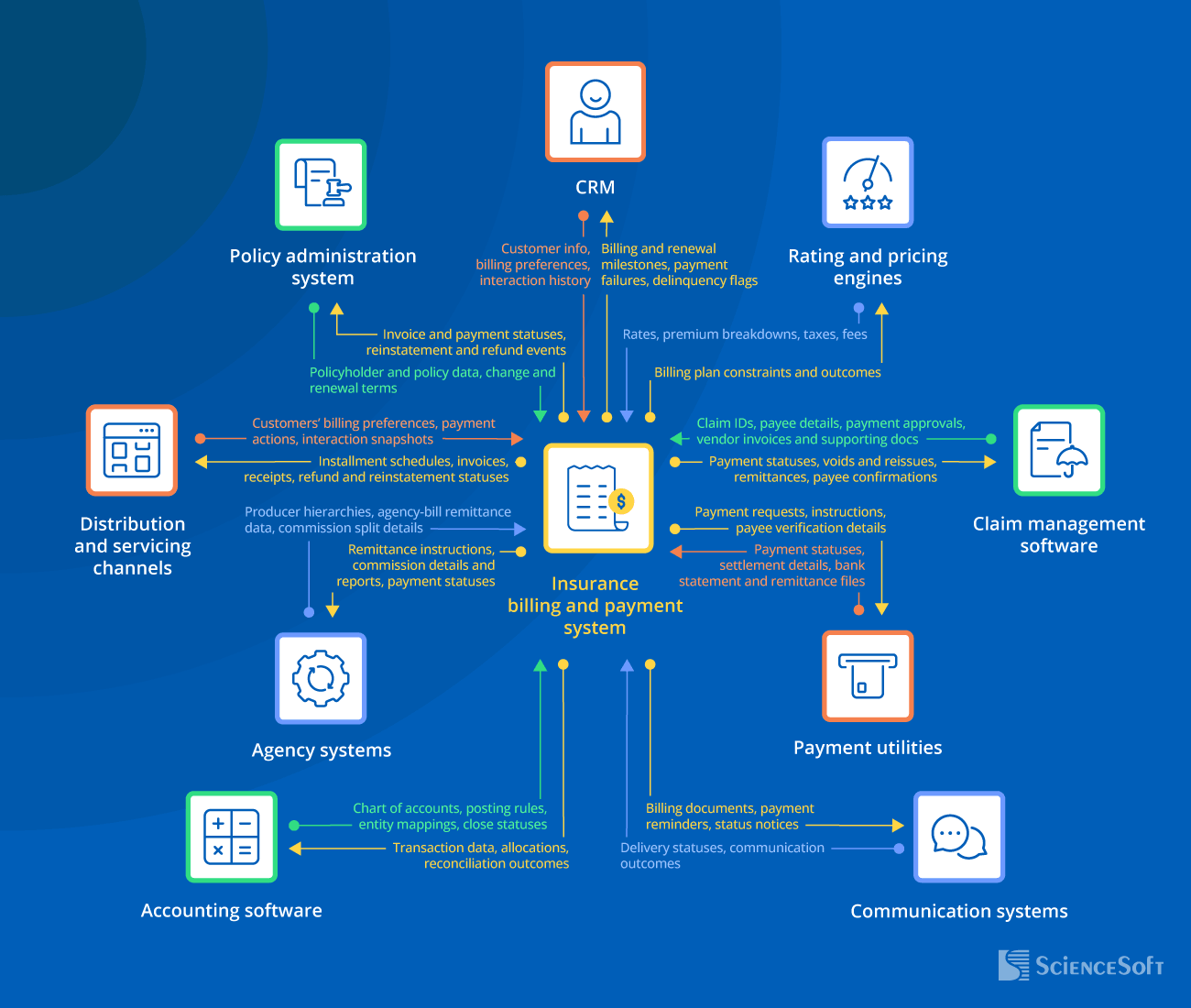

Essential Integrations for Insurance Billing and Payment Systems

To keep billing aligned with policy details, quickly capture policy lifecycle events, and consistently enforce coverage adjustments and terminations.

Rating and pricing engines

To calculate customer invoices based on the current rates and jurisdiction-specific taxes and fees, automate premium delta calculations for mid-term rate changes, and share rating-relevant billing performance insights.

Custom software or enterprise CRM platforms (e.g., Salesforce, Microsoft Dynamics 365).

To auto-populate premium invoices with customer data, trigger outreach at billing moments (e.g., payment failure, renewal billing), and initiate early interactions for delinquent accounts.

To accelerate claim document intake, payouts, and payment status reporting to adjusters.

NB: If you want straight-through settlement for simple claims and disbursement reporting directly to vendors, consider additionally integrating payment software with your vendor portal or vendor networking platforms.

Agency systems

E.g., agency management platforms, agent portals, commission tracking engines.

To speed up remittance advisory, posting, and reconciliation, accurately calculate commissions, streamline commission reporting, and keep agencies updated on payment statuses.

NB: This integration lets carriers expose automated billing functionality directly to partner agents.

Payment utilities

E.g., payment gateways, bank systems, direct debit services, disbursement networks (ACH/SEPA, push-to-card, e-check, etc.).

To automatically process premium, commission, and claim payments, track real-time payment statuses, speed up settlement posting and reporting, and handle payment retries and returns.

For straight-through transaction posting in the insurer’s accounting ledgers and faster financial close.

NB: Direct integration between an insurance billing system and a revenue management system streamlines service-based insurance revenue recognition under ASC 944/IFRS 17 and ASC 606/IFRS 15 models.

Communication systems

E.g., email, SMS, and instant messaging services; call center systems.

To streamline customer, agent, and partner communications around billing and payment events, improve collections conversion, and give call center agents real-time access to contextual data for billing-related interactions.

Best Practices for Insurance Billing and Payments Software Development

Below, ScienceSoft’s experts share their best practices for engineering reliable and cost-effective insurance billing and payment systems.

![]()

Define control points for exceptions before automating

In insurance billing and payment workflows, the biggest control risks usually appear in exceptions: refunds, reversals, payment retries, commission corrections, claim payout changes, and other manual interventions. If these scenarios are not designed with clear permissions, approval rules, and audit trails from the start, automation can create operational risk instead of reducing it.

That’s why at ScienceSoft, we gather the insurer’s requirements and applicable regulatory rules for who can initiate, approve, override, and reprocess each financial action and what evidence the system must retain at the early planning stages. By doing this, we ensure that the solution will be designed to support day-to-day financial control, internal audit, and compliance requirements from the start. Early validation of exception logic with the client’s stakeholders is how ScienceSoft secures the accuracy of custom financial solutions.

Since core permission, exception, and compliance controls must already be in place in the MVP, early planning also accelerates feature scoping and shortens time to production.

![]()

Architecture should be designed for fast, cost-efficient scaling

Month-end billing, commission payment bursts, catastrophe-driven payouts, and mass reconciliation runs create predictable spikes in billing and payment system load. Handling these fluctuations efficiently requires an architecture that sustains high performance without permanently overprovisioning infrastructure.

ScienceSoft’s principal architects suggest that cloud-based modular architectures with selectively applied serverless components are particularly effective for such scenarios. Serverless functions execute only when triggered and scale automatically on demand, making them well-suited for automating cyclical billing and payment workflows without paying for idle compute capacity during off-peak periods.

Multi-functional insurance payment management systems can also benefit from event-driven architectures, where billing and payment events are sent to a central hub that routes them to the appropriate software components for processing. This design enables smooth concurrent handling of high-volume recurring workflows across invoicing, payouts, transaction recordkeeping, and reporting.

![]()

Rigorous functional testing is critical for accurate automation

QA engineers at ScienceSoft target 90%+ overall unit test coverage and 95%+ coverage for back-end components responsible for data integration, financial calculations, invoice and payment routing, reconciliation, and fraud detection. Based on our experience, coverage below these benchmarks doesn’t provide sufficient validation for financial logic and integrations and increases the risk of defect leakage into production. Test-driven development is a natural fit to support this level of coverage; however, we always consider each project’s unique constraints to choose the optimal QA strategy.

The test suite should incorporate the insurer’s real transactional data patterns and operational scenarios. Particular attention must be paid to edge and corner cases, such as mid-term endorsements, failed, partial, and duplicate payments, chargebacks, reversals, reinstatements, and out-of-order processing events. Testing at this depth ensures the billing and payment solution performs accurately and consistently in real-world conditions.

Costs of Insurance Billing and Payments Solutions

Developing insurance billing and payment software may cost from $100,000 to $1,800,000+, depending on the solution’s functionality, the scope of supported product lines and jurisdictions, the number and complexity of integrations, as well as performance, scalability, and security requirements.

Here are ScienceSoft’s sample cost ranges for common development scenarios:

![]()

$100,000–$400,000

A focused process improvement module, such as payment orchestration, payment document processing, fraud detection, automated reminders, or premium payment self-service, integrated with one or two core insurance systems.

![]()

$150,000–$600,000

A custom solution that automates a specific insurance finance function end-to-end (e.g., billing, commission management, claim payment). We can implement it as a module in the core platform or as a standalone tool integrated with other systems.

![]()

$500,000–$900,000

A multi-module modernization initiative covering billing, collection, commission management, reconciliation, and servicing workflows across one traditional insurance line. We deliver the new modules in phases and integrate them with PAS, claims tools, accounting software, and payment utilities.

![]()

$900,000–$1,800,000+

A large-scale custom billing and payments platform for multiple insurance products, premium collection models, payment channels, and partner flows. It can support AI-driven automation, real-time analytics, risk management, and complex integrations across the insurer’s operating landscape.

* The estimates are for mid-sized insurers (<2,000 employees) serving 1–5 traditional insurance lines. The final implementation cost will depend on the insurer’s specific needs, the maturity of the firm’s IT ecosystem, and the complexity of data migration procedures.

Wondering How Much Your Software Project Will Cost?

Why Develop Insurance Billing and Payment Software With ScienceSoft

- Since 2012 in engineering custom software solutions for the insurance industry.

- Since 2007 in corporate financial software consulting and development.

- Insurance IT and compliance consultants (NAIC, HIPAA, NYDFS, GDPR, etc.) with 5–20 years of experience.

- 45+ certified project managers (PMP, PSM I, PSPO I, ICP-APM) who succeeded in large-scale projects for Fortune 500 firms.

- 9 principal architects with hands-on experience in designing complex finance automation systems and driving secure implementation of innovative technologies.

- 350+ software engineers, 50% of whom are seniors or leads.

- Established practices to ensure the high quality of insurance solutions and their delivery on the agreed timelines and budget, despite project constraints or uncertain requirements.

ScienceSoft’s approach, as seen through our clients’ eyes

ScienceSoft demonstrated a deep understanding of our requirements, and their insurtech developers needed minimal supervision.

What stood out was ScienceSoft's proactive suggestions for cost-saving architecture design and tech stack solutions. Their input ensured we stayed within budget without compromising on software quality. The value we derived from partnering with ScienceSoft is definitely worth the investment.

Partnering with ScienceSoft has been an excellent experience. Their team transformed our underwriting platform into a well-oiled machine. They identified and fixed several longstanding issues that had been causing us persistent difficulties. Their communication was exemplary; unlike our previous experiences with outsourcing, we never had to chase them for updates, and they were always prompt in responding to our queries.

Damien Sewell

Head of IT Projects

ScienceSoft’s quick buy-in and readiness to take the initiative made the project faster and less stressful for everyone involved, from Capital IM’s insurance specialists to leadership. At the end of a short yet highly productive two months, we got a secure and wholly owned property insurance solution that is fully adapted to Capital IM’s corporate practices and brand book. We couldn’t have asked for a better IT partner.