Artificial Intelligence (AI) in Insurance

Opportunities, Use Cases, Technical Design

In insurance IT since 2012 and in AI engineering since 1989, ScienceSoft helps insurance market participants and insurtech firms create tailored insurance AI solutions. Our architects design secure and scalable AI architectures that integrate with the existing insurance software systems while supporting safe, accurate, and controllable AI automation.

in Insurance - ScienceSoft")

Contributors

Senior Insurance IT & AI Consultant, ScienceSoft

Head of AI, Principal Architect, ScienceSoft

Financial Technology & AI Researcher, ScienceSoft

Key Opportunities Artificial Intelligence Unlocks for Insurance

Artificial intelligence (AI) solutions for insurance can automate complex submission processing, risk analytics, and reasoning tasks, provide real-time decision support, and streamline multi-step workflows across underwriting, policy servicing, and claims. ScienceSoft is an AI development company that serves the insurance industry.

82% of insurance businesses that adopted AI report its early positive impact on business revenue. The gains are typically realized through higher operational speed and efficiency, enhanced employee capacity, tighter risk pricing, lower fraud-related losses, and higher customer satisfaction. ScienceSoft can develop insurance software with built-in AI capabilities to support agents and policyholders.

Here’s how the adoption of AI insurance technology is projected to reflect on the industry in the coming years:

- BCG estimates that AI can reduce P&C insurers’ operational costs per dollar of premium by 15–25%, which, in the US alone, equates to $35–60 billion in reduced operating expenses. The firm found AI can also increase premium per policy, with leaders in AI adoption in the US projected to win an extra $8–20 billion.

- Forrester, in its US Insurance Tech Spending 2026 outlook, highlights AI as a critical lever for insurer profitability in a tightening pricing environment, projecting that broader adoption could improve insurers’ expense ratios by up to two points.

- Deloitte estimates that implementing AI and real-time analytics across the claim life cycle will help P&C insurers save $80–160 billion by 2032 due to improved fraud detection.

Three Major Types of AI Applied in Insurance

![]()

Machine learning (ML)

Traditional AI technology used in predictive risk analytics, anomaly detection, and insurance modeling and optimization engines. ScienceSoft is an insurance AI application development company building custom AI-powered tools for insurers.

![]()

Generative AI

Mainly, large and small language models that support unstructured data processing, conversational assistance, content creation, and decision support. ScienceSoft can modernize insurance platforms by adding generative AI capabilities for agents and policyholders.

![]()

Agentic AI

Highly autonomous systems that can orchestrate and execute insurance workflows end-to-end, often by engaging multiple ML and GenAI components.

AI in Insurance: Market Summary

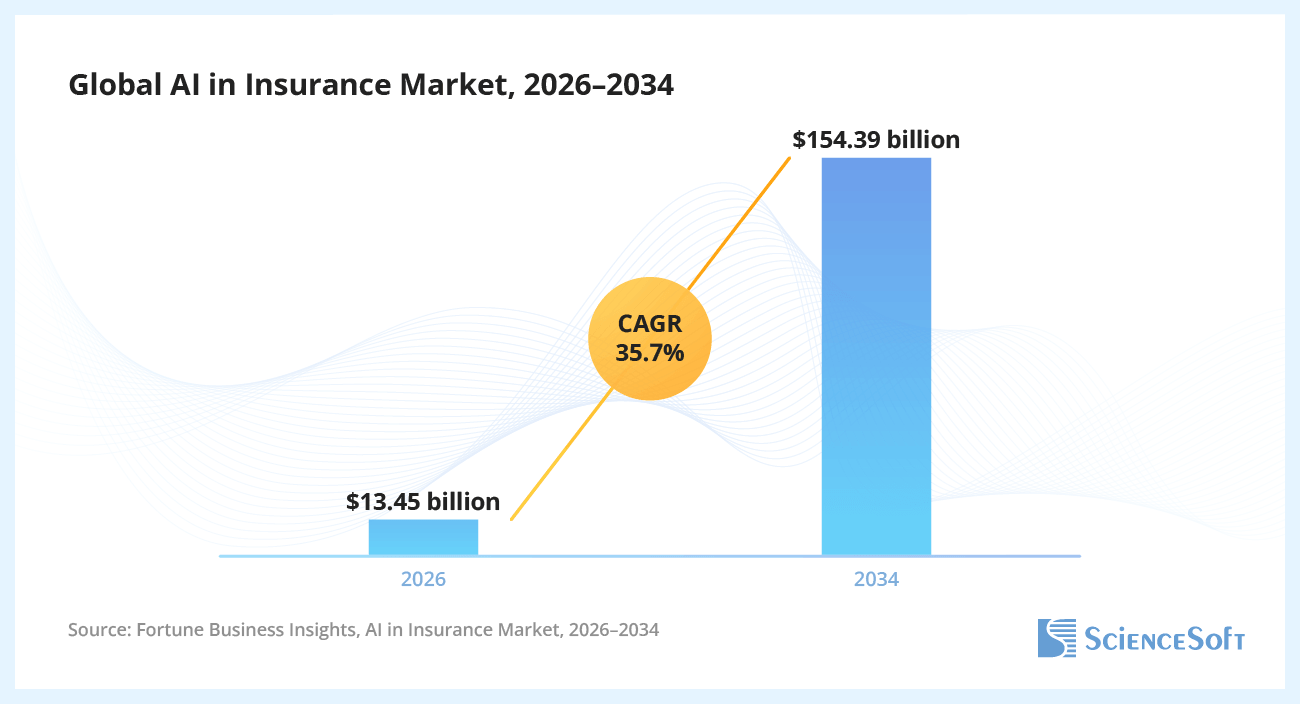

The global market of artificial intelligence in insurance is projected to grow from $13.45 billion in 2026 to $154.39 billion by 2034 at a CAGR of 35.7%.

The segment of machine learning technology captured the largest market share (46%) in 2025. Natural language processing (NLP), the second-largest market segment, is anticipated to post the highest CAGR (39.4%) by 2034 due to the rise of generative AI and large language models (LLMs), which fall under the broader NLP umbrella.

Fortune Business Insights names generative AI a major catalyst for the insurance AI market growth in the coming years. The market of generative AI in insurance is anticipated to grow 9x and reach $10.94 billion by 2034. The market of insurance agentic AI is expected to hit $18.16 billion in 2030, up from zero in 2024.

Entities That Benefit From Building Tailored Insurance AI Tools

Third-party administrators

Distribution facilitators (NMOs, banks, embedded insurance partners, etc.)

Risk management providers

Reinsurers

Latest Trends in Insurance AI Adoption

82% of insurers believe AI will dominate the industry’s future. As of 2026, a vast majority of insurance organizations have already deployed traditional AI/ML for predictive analytics and automation, with NAIC citing an adoption rate of 84% among US health insurers.

Generative and agentic AI are increasingly gaining traction as the next big value drivers. ScienceSoft found that 68% of insurance AI rollouts in late 2025 focused on such solutions. The 2026 report by Earnix highlights that 80% of insurers plan to adopt GenAI by 2028.

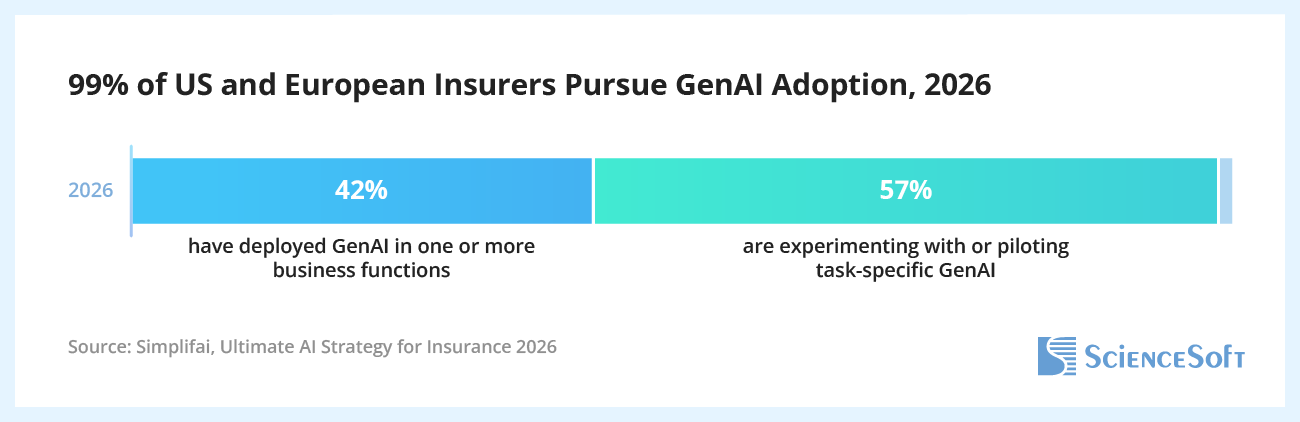

Simplifai’s 2026 report shows that 99% of insurers in the US and Europe have generative AI initiatives underway. 42% of firms report having already implemented GenAI (non-agentic or agentic) for at least one business function and working on further scaling. Among lines of business, property and casualty (P&C) insurers led AI adoption (58.05%) in 2025.

Budget projections prove the industry’s commitment to AI scaling: Accenture’s 2026 Pulse of Change revealed that 90% of insurers plan to spend more on AI in the coming years, with agentic and generative solutions named the top funding priorities.

Key factors driving the popularity of generative and agentic AI in insurance are:

- The demand for more accurate risk assessment and pricing in the face of climate change, cyber threats, and emerging risks.

- The need to accelerate claim processing while reducing reserve leakage and improving fraud detection as fraud schemes become more sophisticated.

- Rising operational complexity and growing insurance data volumes, pushing for greater operational capacity without proportional increases in workforce.

- The need to enhance customer experience through faster and more personalized interactions across channels.

- The competitive pressure from insurtech firms and more digitally mature insurance market players who are leveraging AI to offer better services.

- The growing pressure to reduce operating costs and improve workflow efficiency amid tightening margins.

Agentic AI as the Next Big Value Driver: Featured Expert Talks

AI to Cut the Claims Lifecycle From 44 to 1 Day | Presentation at ITIC 2026

Agentic solutions offer unique benefits for the insurance sector — but they also create unique challenges. Watch the presentation by ScienceSoft’s Vital Soupel, Senior Insurance IT & AI Consultant, at the 2026 Insurance Tech & Innovation Conference in Chicago to learn why insurance organizations are increasingly pursuing agentic AI, what’s holding them back, and how agents work in practice.

AI Agents for Insurance Claims Fraud Detection | Presentation at ITS 2025

AI agents are transforming complex claims validation processes that once required extensive adjusters' effort. Watch the presentation by ScienceSoft’s Head of AI, Vadim Belski, from the 2025 Insurance Transformation Summit in Boston to explore how agentic AI can improve claims fraud detection and what insurers need to deploy AI agents smoothly and safely.

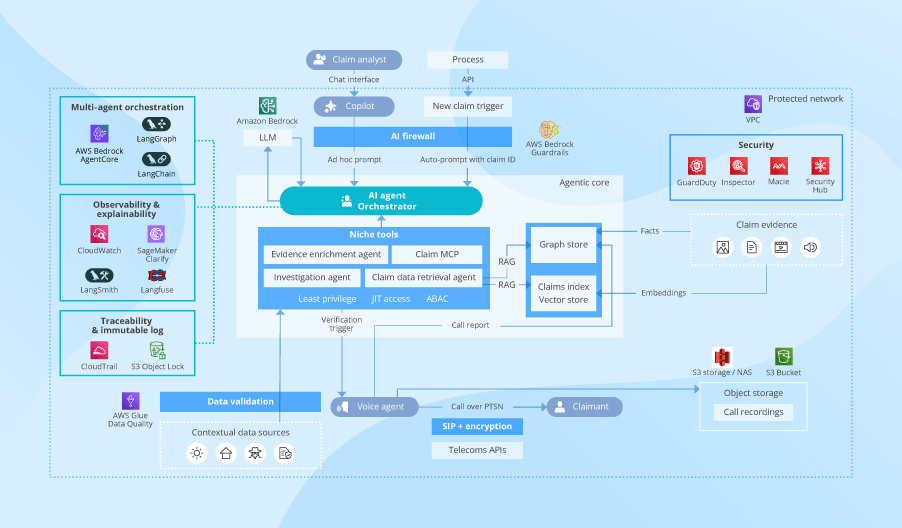

Reference Architecture for Insurance AI Solutions

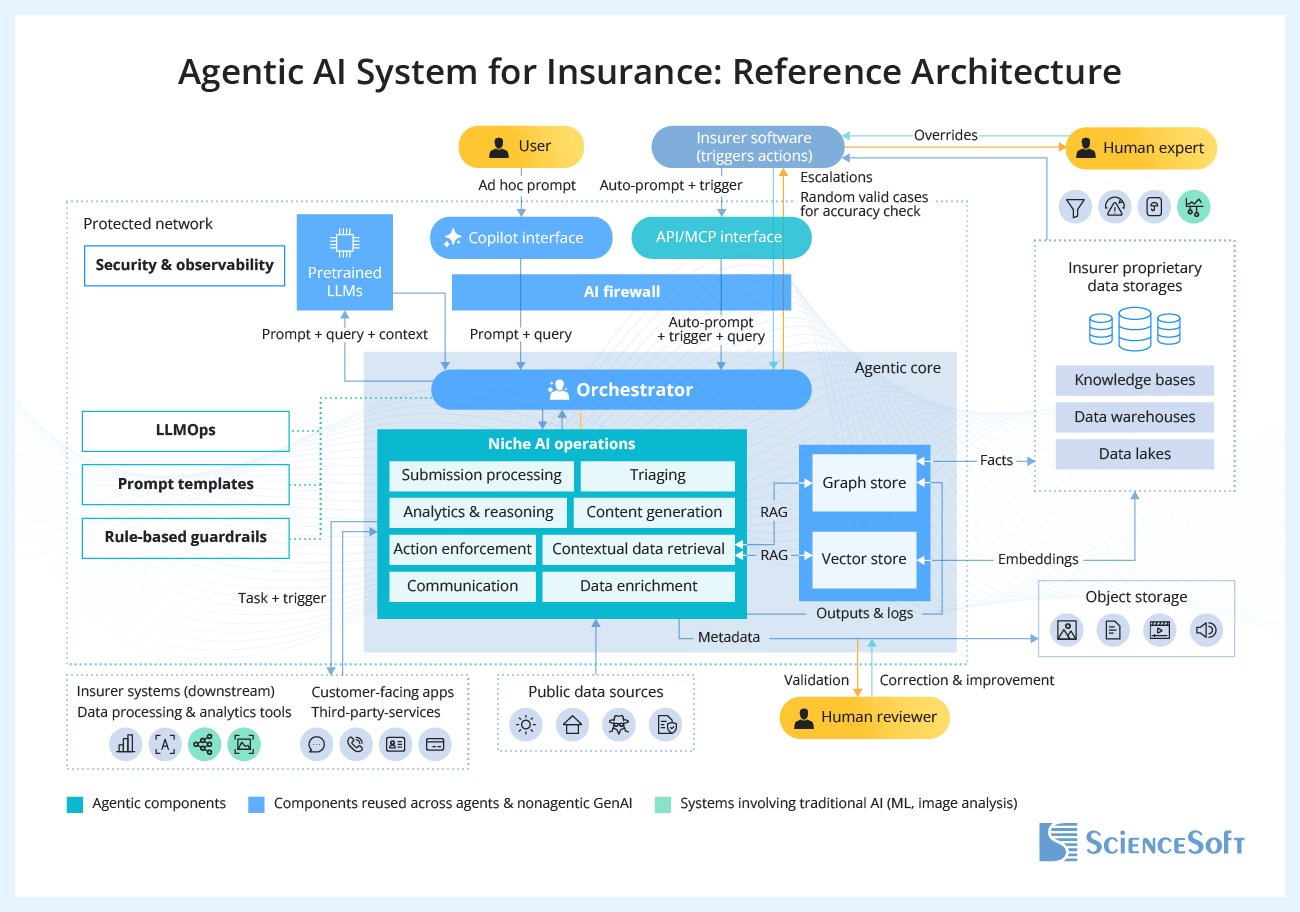

Below, ScienceSoft’s experts share a sample architecture we apply for agentic AI systems in insurance. Originally designed for underwriting and claims workflows at P&C carriers, this architecture can be adapted for administrative, customer-facing, and producer use cases across diverse lines of business.

The blueprint identifies opportunities for component reuse across agentic AI systems and non-agentic assistants, enabling insurance organizations to reduce engineering effort and plan incremental AI expansion more predictably. It also shows how the agents operate within the insurer’s broader software system and interact with traditional machine learning tools.

An agentic architecture isn’t a default for every use case: sometimes, you can get away with much simpler setups. But at the same time, agentic automation is rapidly becoming a target operating model in insurance. Most incumbents we work with are already exploring how to scale from isolated ML and copilot use cases to multi-agent workflows. By preparing the architecture for GenAI, agents, and orchestration from the start, we provide a clear path for evolving AI systems — without overengineering early or having to rebuild the foundation later.

The agentic AI solution communicates with the insurance software systems (underwriting, claims, policy administration, etc.) via API or MCP interfaces. It continuously monitors insurance data and events across the systems, automatically captures tasks and task triggers (e.g., application or claim arrivals), and directs them for validation to the AI firewall. This component enforces security and compliance safeguards, including authorization, PII redaction, prompt-injection checks, and policy-based routing.

In the reference configuration, the agentic system also provides role-based copilot interfaces so users (insurance employees, customers, producers, etc.) can ask questions or submit tasks ad hoc.

After validation, manual and automated queries are forwarded for processing to the orchestrator. The orchestrator serves as the integration and control layer that connects task sources, LLMs, and agentic components and coordinates step-by-step workflows across niche AI agents (for submission processing, reasoning, outreach, etc.). Using narrowly scoped agents instead of a single all-purpose agent helps keep AI logic isolated and easier to test, govern, and update. This also reduces the risk of changes in one workflow affecting others and simplifies control over complex, multi-step agentic operations.

The orchestrator relies on a large language model operations (LLMOps) tool stack to provide event logging and traceability, model logic explainability, and model inference validation. This component also enforces the insurance organization’s rule-based guardrails (execution instructions, approval mandates, etc.) for agentic workflows.

To ground user query responses and task execution in the insurer’s context, the agentic solution pulls contextual data from the insurer’s proprietary data storage. For this, both agents and non-agentic AI assistants rely on retrieval-augmented generation (RAG). The RAG engines retrieve structured, semi-structured, and unstructured insurance data relevant to the request and compile the insights into a unified feed. Where needed, ScienceSoft vectorizes non-structured data in a vector store to make it semantically searchable for the RAG engine.

Since many core insurance workflows are relationship-heavy (customer-producer linking, claim-to-coverage mapping, fraud ring detection, etc.), our engineers may also normalize structured data in a graph store to ensure reliable agentic reasoning over dependencies.

If necessary, the agents perform contextual data search across public sources (open databases of local authorities, risk data platforms of trusted providers, etc.) to enrich the insurer’s internal findings, e.g., when profiling risks or validating claims. They can also select and call the relevant data processing and analytics components, including image analysis and machine learning models, to interpret and validate multi-format ad hoc submissions.

The orchestrator combines the gathered contextual data with the original prompt and assembles an LLM-ready prompt using pre-engineered prompt templates tailored to the insurer’s specific operations. The prompt is routed to the integrated pretrained LLM (e.g., GPT-5, LLaMA, Claude, an insurance-specific small language model). The language model analyzes the prompt and responds with links to the source data and citations. The response is logged and validated in the orchestrator and, if accurate and relevant, submitted to the user or to the agents to inform further automation workflows.

Based on the LLM outputs, the niche agents take action: compose insurance documents, distribute notifications via customer apps, make calls and summarize outcomes, or trigger insurer systems and third-party services to execute specific tasks, e.g., KYC screening, quote drafting, routing approved claims for payout. The orchestrator involves the LLM after each agentic iteration to reason on the results and next steps. If the predefined authorization guardrails demand human approval or the LLM output is ambiguous, the agent escalates the task to the human expert.

Human reviewers receive agentic outputs that need approval as auditable artifacts (data summaries, citations, proposed steps, and confidence scores). The orchestrator captures review results and triggers automation for approved workflows. The approved agentic outputs are written to the databases and, where applicable, to the graph store to be available for the insurer’s operating systems. Semi- and non-structured files (e.g., AI-generated documents, tables, images, call recordings) are directed for retention and reuse to the dedicated object storage.

The convenience of this setup lies in its flexibility and enterprise fit. It allows insurers to add AI on top of their existing workflows without replacing existing systems. The modular design makes it easy to combine best-of-breed LLMs, orchestration frameworks, and cloud services, reducing vendor lock-in risk while keeping options open for cost and performance optimization. The same modularity also makes it easier to extend the system with new specialized agents and integrations as business needs evolve.

Another key advantage is robust controls. The AI firewall and LLMOps capabilities provide end-to-end visibility into agent behavior, making intelligent decisions easier to trace, explain, and audit. This supports compliance and builds trust with business users. With customizable guardrails, insurers can set up agentic execution rules tailored to their internal policies and regulatory constraints. Separation of agent duties also allows firms to enforce task-level permissions, which helps contain risk and simplifies governance. Since each agent gets its own compute resources, you can better control the type and volume of resources they receive and avoid overprovisioning.

Practical AI Applications in Insurance

Drawing on decades of experience in artificial intelligence and recent insurance technology projects, ScienceSoft’s consultants list the insurance functions where AI can deliver the biggest value, starting from the most prominent application areas.

The biggest impact doesn’t always mean the best place to start. Yes, AI in underwriting, claims settlement, and fraud detection brings the highest ROI when done right. But it also comes with the heaviest complexity, regulatory scrutiny, and the need for mature governance, validation, and human-in-the-loop controls.

That’s why I usually suggest starting AI pilots in either front-line assistance or cross-functional routines like data intake and summarization. These are lower-risk, lighter on data preparation, and more contained in scope, which makes them the easiest environments for testing, deploying, and refining AI. Just as importantly, they show value fast, helping build user confidence and giving leadership a clear signal to scale AI further.

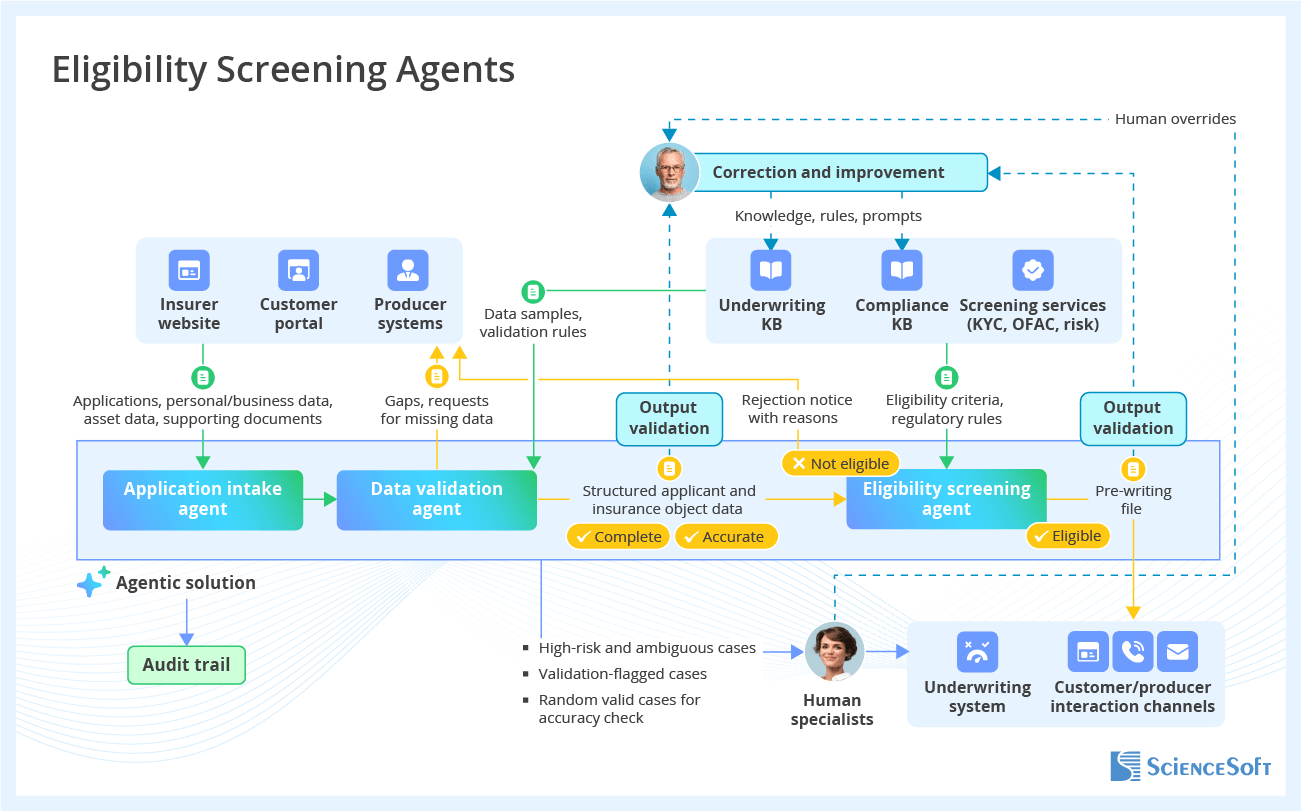

AI for insurance underwriting

Generative AI tools can extract data from applications, perform eligibility screening, and generate concise case and risk summaries. Agentic AI pipelines, combined with ML models for risk assessment and premium optimization, can automate straight-through underwriting for standard cases. Agents can also assist underwriters with decision-making in complex scenarios and orchestrate the entire underwriting lifecycle across systems.

How AI works for underwriting

Image analysis and LLM engines automatically extract and structure data from insurance applications (ACORD, EDI, custom forms, etc.) and supporting documents. Machine learning models and LLMs validate submissions for accuracy and completeness and trigger requests for missing customer data. They also enrich risk profiles with data from the insurance systems and external sources and handle early application eligibility screening against the company’s product and KYC policies.

For eligible submissions, LLMs summarize case and risk data and compose pre-writing files. ML-powered predictive analytics engines analyze and score risks, highlight key risk drivers, and deliver risk-based pricing suggestions. LLMs consolidate outputs into a final decision or grounded recommendation for the underwriter.

Agentic AI systems coordinate the end-to-end intelligent underwriting workflow, triggering data processing, analytics, and decision support actions. They can enforce straight-through underwriting decisioning and outcome communication to customers and producers for standard cases while routing complex risks for manual handling.

Sample agentic workflow

Reported outcomes

AI has proven to cut risk assessment times from days to minutes, accelerating the time to quote by more than 4x. Early adopters of GenAI in underwriting managed to reduce manual work around data collection and analysis by over 65%, increase underwriter productivity by 100%+, and process up to 40% more applications without increasing headcount. AI-powered predictive risk analytics can bring insurers a 3–10% improvement in loss ratios thanks to more comprehensive risk profiling and sharper personalized pricing. Intelligent decision-making engines can underwrite over 90% of standard applications outright.

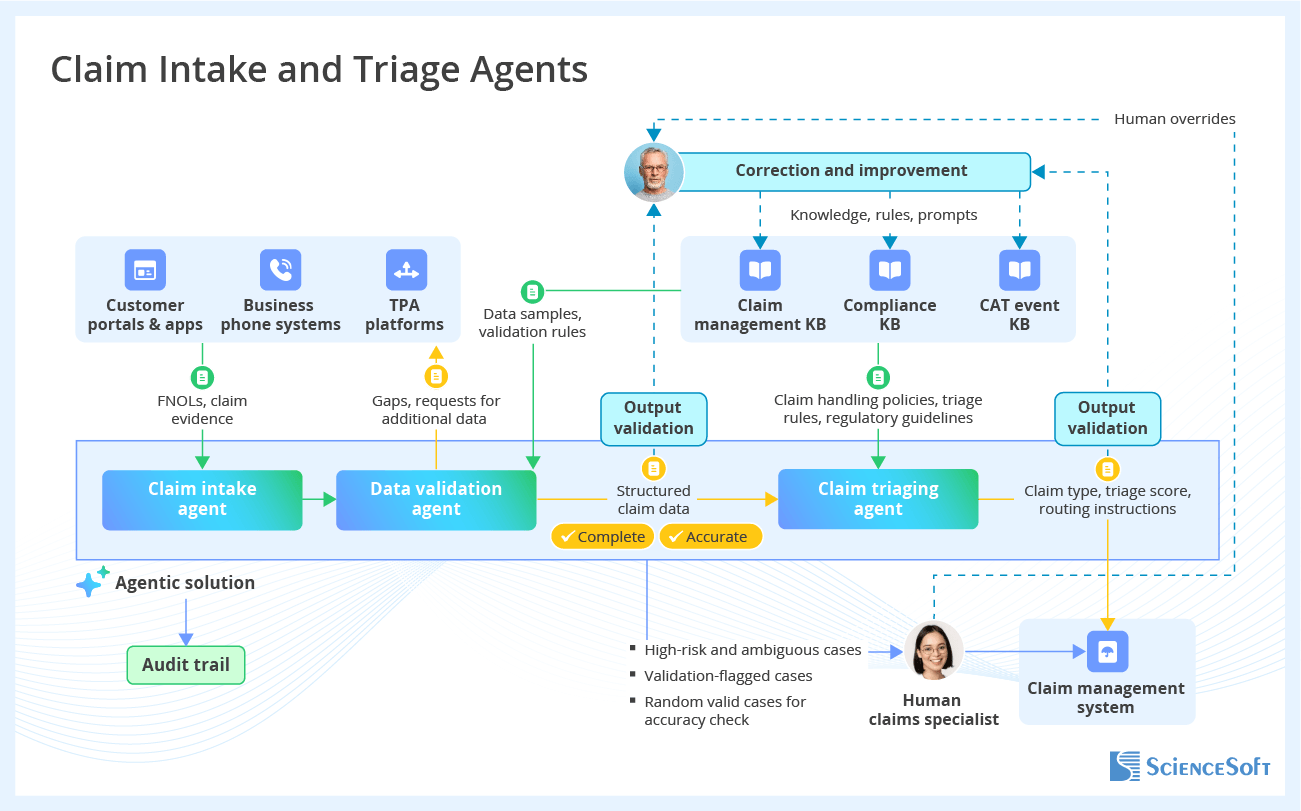

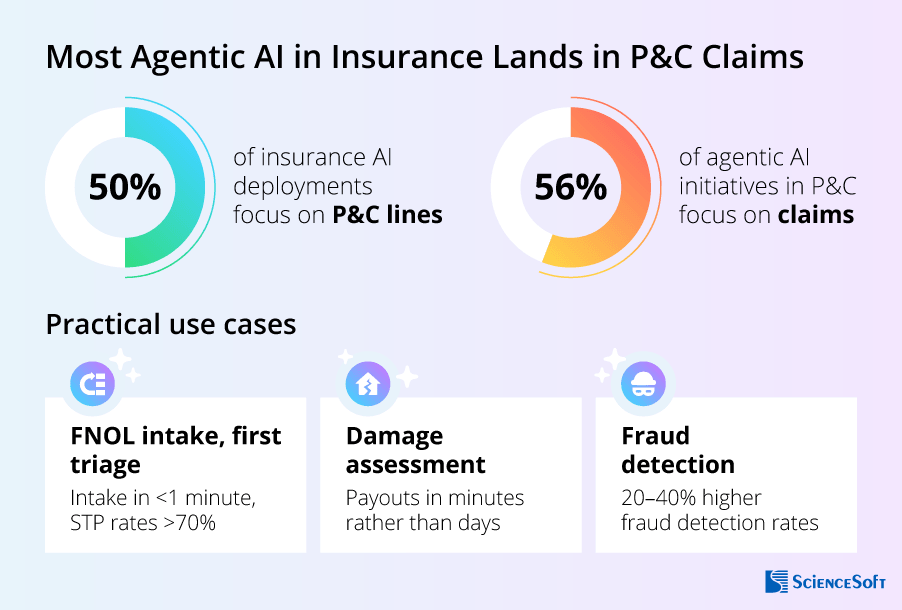

AI for insurance claim management

Generative AI engines can structure incoming claims, validate textual evidence, and produce case summaries. Image analysis algorithms can be applied to validate image and video evidence. Building on this, predictive ML models can handle automated damage assessment and reserve estimation. Agentic AI layers can then coordinate triaging, automate settlements for simple cases, support adjusters in complex decisions, and curate the full claims lifecycle across systems with minimal manual handoffs.

How AI works for claim management

LLMs automatically retrieve and structure claim data from FNOLs and multi-format claim evidence (documents, photos, videos, handwritten notes, etc.). Specialized AI algorithms (e.g., medical image analysis, motion capturing) and ML-powered predictive analytics vet media files for authenticity and case relevance and trigger outreach for gapped submissions. GenAI engines enrich claim data with the customer’s policy details, past interactions, and insights from external sources (medical databases, telematics databases, weather platforms, etc.).

Once the claim is structured, ML models estimate claim severity and payout amounts. They match the claim against coverage terms and past cases, determine the appropriate handling path, and triage claims for settlement. LLMs pack claim details and proposed settlement scenarios into decision-ready claim files, augmenting them with suggestions on claim negotiation tactics, execution vendors, and disbursement time windows.

The agentic workflow orchestrator coordinates next steps, such as triggering onsite inspections, involving partners, proceeding with straight-through settlement, or routing complex cases to human adjusters.

Sample agentic workflow

Reported outcomes

AI-supported automation can drive up to a 50% increase in adjuster productivity and a 20–50% reduction in claim handling costs by streamlining claim intake, validation, and assessment. It can drive more than 50x faster processing of complex claim documents, cutting claim cycle times from weeks to minutes and improving policyholder satisfaction rates by over 10%. With GenAI-supported damage assessment and settlement planning, insurers and TPAs can reduce claim leakage by 30–50%. Intelligent decision-making and agentic automation can support straight-through resolution for up to 70% of simple claims.

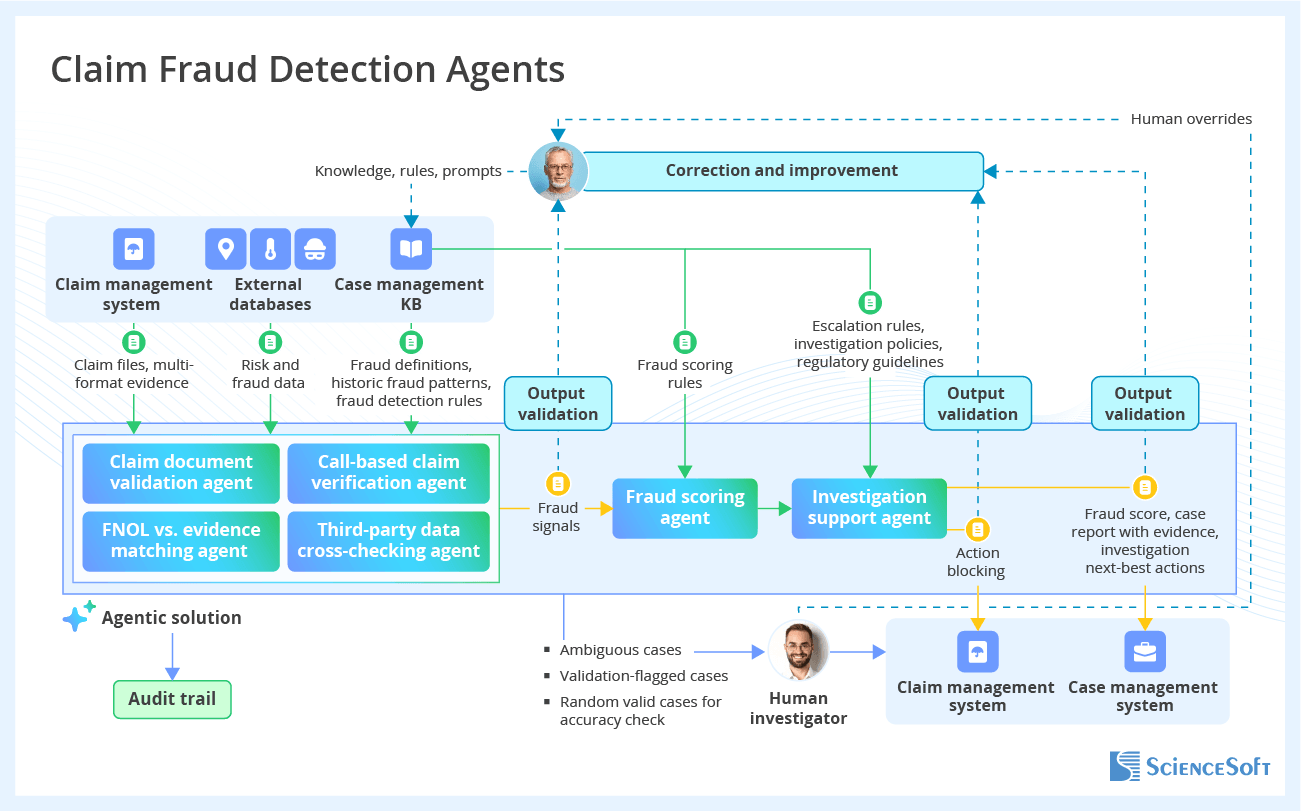

AI for insurance fraud detection

ML models form the backbone of automated insurance fraud detection: they can continually monitor data and behavioral patterns, flag risks, and uncover complex, multi-party fraud schemes. GenAI can detect forgery across unstructured evidence, handle conversational case verification, and generate case summaries and reports. AI agents can coordinate investigations, trigger fraud alerts, and automate end-to-end fraud detection workflows across systems. ScienceSoft can build a fraud detection AI agent for insurance to help identify suspicious claims faster.

How AI works for fraud detection

LLMs analyze multi-format documents and unstructured communications, including customer responses during live calls, and instantly spot inconsistent responses or evasive wording that may indicate fraud. In parallel, GenAI, image analysis, and natural language processing algorithms handle media file validation and identify likely edited, reused, staged, or entirely fabricated evidence. ML-driven graph analytics engines monitor relationships among customers, producers, and damage-handling partners and capture network collusion signals.

Diagnostic and predictive ML models continually analyze the revealed behavioral deviations and technical forgery, define fraud type, and score fraud probability and severity. LLMs summarize findings and generate investigation-ready case reports with clear explanations of detected risks.

AI agents can coordinate and automate fraud detection and investigation, engage relevant analytics tools, handle verification calls, and escalate high-risk cases to investigators. Following SIU instructions, they can auto-enforce fraud response, e.g., temporarily block suspicious claims for settlement or alert partner relationship specialists about network concentration.

Sample agentic workflow

Reported outcomes

AI enables insurers to spot fraud across applications, claims, and multi-party interactions faster while improving fraud detection accuracy by 20–40%, compared to traditional rule-based methods. Intelligent automation of submission checks and investigation workflows can drive an up to 5x increase in investigator capacity and save 20–40% in fraud detection and investigation costs. AI-enabled early blocking of illegitimate and inflated claim payouts can reduce fraud-associated claim losses by 5–20%.

AI for insurance risk mitigation

Predictive ML models can continuously monitor exposures and spot emerging threats, including catastrophic risks. Generative AI can enhance this by translating risk signals into actionable insights, enabling guided mitigation planning and personalized customer advice on loss prevention. AI agents can trigger risk alerts and coordinate proactive risk management workflows across portfolios.

How AI works for risk mitigation

Machine learning models for predictive risk analytics handle continuous monitoring of general and catastrophic risk exposure after policy issuance. They track changes in customer behavior, asset conditions, and external factors (environmental, geopolitical, etc.), spot emerging risks and concentration patterns, and flag them for proactive actions.

Underwriters and risk analysts can ask GenAI assistants to interpret and prioritize exposures and suggest targeted mitigation actions based on similar cases and portfolio trends. Upon request, LLM engines also draft personalized guidelines for policyholders on safety improvements, asset maintenance actions, and behavioral changes to prevent losses.

AI agents can automatically capture emerging exposures, notify risk management stakeholders, trigger reviews of AI-generated mitigation suggestions, and enforce the distribution of advice across customer channels.

Reported outcomes

AI enables insurance incumbents to move from periodic risk assessment to continuous risk monitoring and proactive mitigation while driving more than 60% productivity gains across perpetual risk data gathering. It helps reduce loss frequency and severity by identifying emerging risks early. Intelligent recommendations on risk prevention actions give organizations the opportunity to improve customer loyalty through value-added loss mitigation services.

AI for insurance employee assistance

GenAI copilots can retrieve insurance knowledge, summarize policies and cases, and draft documents, customer communications, and educational content. They can provide context-aware recommendations for insurance decision-making, including real-time guidelines for call center teams. AI agents extend this by independently taking low-risk, high-volume actions (e.g., mass notifications or policy updates) on behalf of employees.

How AI works for employee assistance

Insurance employees can ask conversational assistants to navigate multiple insurance knowledge bases and external sources, parse relevant data and documents, extract and summarize findings, and provide structured answers in the requested format. GenAI copilots can craft simple explanations of complex terms and clauses, highlight key points, and suggest best next actions for decision support inquiries. They can produce case summaries, insurance documents, reports, knowledge articles, and customer messages based on the context and structure provided by the staff.

Following minimal ad hoc instructions, AI assistants with agentic capabilities can create and schedule tasks, update information across connected systems, trigger insurance automation workflows, and coordinate multi-step operations across several functions (e.g., quoting — binding — billing).

Reported outcomes

Generative AI assistants have proven to boost the productivity of insurance teams by more than 30% by simplifying access to information and reducing time spent on routine data processing tasks. They can cut time spent on data search and summarizing by up to 50% while improving the relevance of insights. Intelligent assistance helps streamline onboarding for new employees, accelerate customer servicing, and drive faster, more consistent decision-making.

AI for insurance customer service

Generative AI assistants enable 24/7 support for insurance customers, handling omnichannel inquiries, guiding insureds through applications and claims, and delivering personalized coverage recommendations. They can proactively engage customers with relevant updates and reminders while assisting servicing teams with real-time insights and response suggestions. Agentic assistants can automate end-to-end service request handling.

How AI works for customer servicing

AI-powered chat and voice assistants capture plain-language customer requests across digital and call center channels in real time. LLMs extract key information, recognize intent, and generate accurate, context-aware responses. They interact with the insurance knowledge bases and operating systems via RAG to retrieve product information, policy data, submission statuses, and customer interaction history. When customer input is unclear or incomplete, assistants can ask follow-up questions, clarify inputs, and request additional data. Following established guardrails, AI hands off any complex, sensitive, or low-confidence requests to humans with full conversation context.

Agentic assistants can take reactive action without human involvement. They can coordinate and automate workflows like updating customer personal data, recording FNOLs, initiating claim processing, and distributing approved insurance documents. AI agents can also proactively engage with customers, e.g., by sending renewal reminders, notifying them of claim status changes, or recommending policy updates based on life events and behavioral signals.

Reported outcomes

By minimizing reliance on human agents for routine interactions, GenAI-powered assistants can cut customer servicing costs by up to 70%. They can automatically handle 50–90% of simple customer inquiries, reduce average handling time by 30–50%+, and cut after-interaction work by up to 20%. Insurance organizations employing GenAI and agentic assistants report a 3–45% improvement in customer satisfaction rates achieved through faster, more consistent responses.

AI for insurance sales support

For agencies and brokers, generative AI can automate lead processing, qualify opportunities, and draft tailored proposals and client communications. GenAI assistants can guide producers through quoting workflows and suggest next best actions during customer conversations. With ML-powered analytics, producers can surface demand and sales insights to improve positioning and highlight optimization opportunities. Agentic AI can automate workflows across the sales cycle.

How AI works for sales support

LLM engines capture and structure customer and risk data from insurance applications, supporting documents, and related conversations. They validate submissions for completeness, consistency, and authenticity, involving machine learning models in forgery detection, and enrich customer profiles with the producer’s internal data and external insights. Next, LLMs verify lead eligibility against carriers’ product rules and underwriting guidelines and triage leads for handling.

For eligible opportunities, AI agents automate standardized workflows (aligned with ACORD, EDI, etc.) across application packaging, new business placement, and carrier quote intake. LLMs can also compare offerings from multiple carriers and highlight options that match the customer’s profile best. They analyze coverage gaps and suggest personalized upselling strategies with optimal product bundles. Such tools produce customer-ready proposals, coverage explanations, and outreach messages, tailoring the tone and style to each prospect’s stated preferences and interaction history.

Agentic systems capture quote confirmations, initiate binding, distribute invoices and policy documents, and register sales transactions in AMS/CRM. Predictive analytics models evaluate sales results and suggest ways to improve conversions and process efficiency.

Reported outcomes

By helping insurance agents and brokers discover opportunities faster, understand customer needs better, and engage customers with more relevant offers, generative AI can drive, on average, a 5–8% increase in sales and cross-sell conversion rates. It can draft customer outreach materials up to 50% faster, boosting producer productivity by an additional 15%. Agentic automation enables up to 70% faster quote turnaround through quicker application processing and quote compiling.

AI for insurance billing and payments

GenAI engines can validate insurance payment data, reconcile transactions, and draft financial documents and context-aware financial communications. Predictive machine learning models help assess payment risks and identify optimization opportunities across billing cycles and claim payouts. Agentic capabilities enable end-to-end orchestration and automation of billing and payment processes.

How AI works for billing and payments

OCR and rule-based algorithms capture standard fields and structured financial data from insurance payment documents. ML-supported data processing engines classify document types and flag anomalies that may indicate data gaps or potential forgery based on learned examples. LLMs extend these capabilities by interpreting unstructured payment files, extracting context from complex documents, and detecting subtle inconsistencies and fraud.

Generative AI copilots can help billing and payment teams retrieve financial data, plan payments and collections, and draft communications. They can also draft invoices, commission statements, and payout instructions in alignment with the insurer’s payment terms.

Predictive analytics engines dynamically track and forecast cash flow, reconcile financial transactions, and flag risks and anomalies that require manual handling. They analyze premium, claim, and commission payment flows and provide suggestions on ways to optimize transaction costs and mitigate delinquency risks.

AI agents can orchestrate the full transactional workflow and trigger premium collections, claim payouts, and commission distributions in compliance with the insurer’s instructions, approval mandates, and regulatory constraints. They automatically resolve known exceptions and escalate complex cases for manual handling.

Reported outcomes

AI can cut billing and collection costs by more than 40% and settlement processing costs by up to 80%, thanks to faster and more efficient operations. By combining machine learning and generative AI, organizations can accurately allocate and reconcile 60%–80%+ of payments, including remittance-less transactions, without human involvement. Early adopters of agentic AI in claim payments have reported 95% auto-payout rates and 70% of disbursements completed within 12 hours after FNOL.

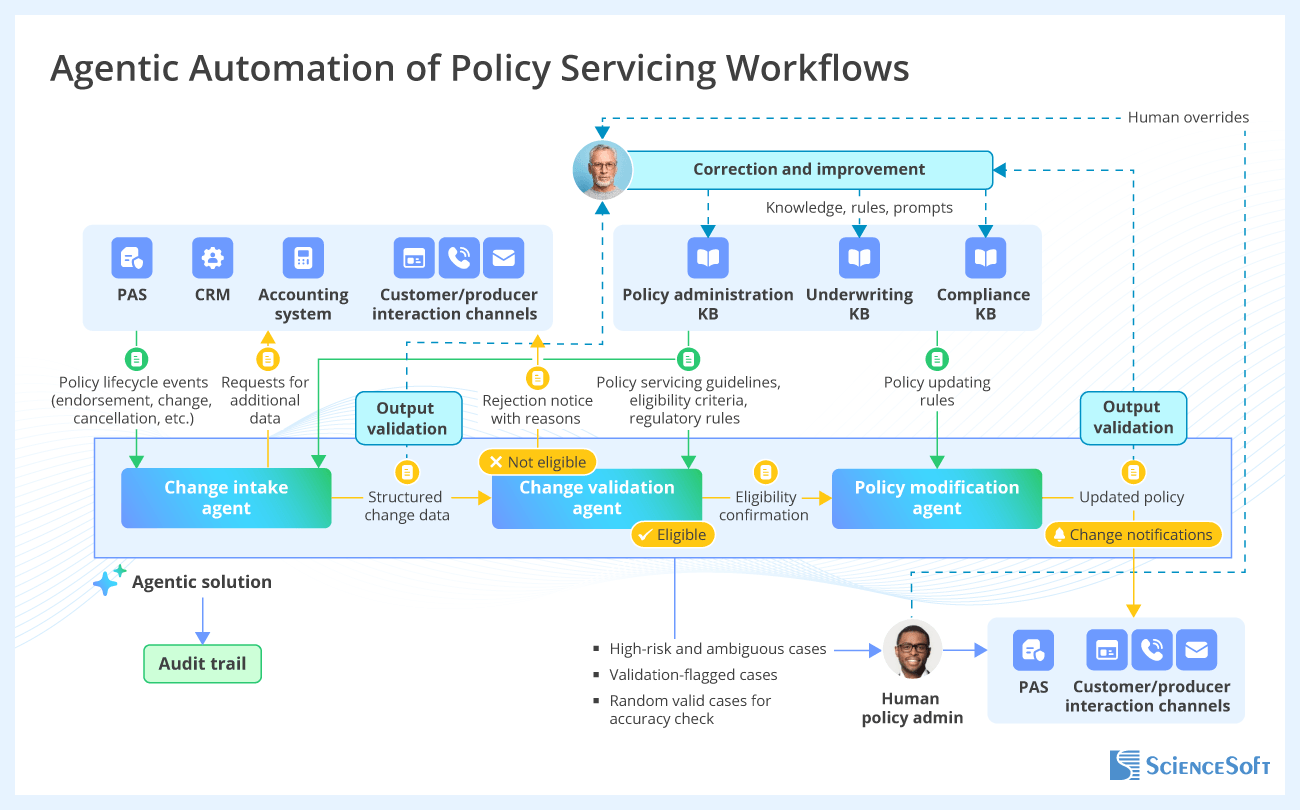

AI for insurance policy administration

Generative AI can automatically assemble insurance policy documents, process policy renewal and change requests, and produce engaging policyholder communications. Machine learning models can dynamically validate policy data and records across systems. Agentic automation tools can coordinate end-to-end policy administration processes, enforce policy lifecycle events, and trigger omnichannel customer outreach.

How AI works for policy administration

LLM engines draft personalized policy documents, endorsements, and policy-related customer communications. Machine learning validation models double-check policy data for consistency and compliance and handle periodic, selective policy reviews. When a renewal or change to the policy is needed, LLMs extract and structure information from textual and voice customer requests, submitted documents, and producer inputs, and generate updates to policy records.

GenAI assistants guide policy administrators on winning customer outreach timing and channels for policy renewals. They can craft engaging renewal offers and suggest policy adjustments based on customer profile and behavior changes.

Agentic AI orchestrates the entire policy lifecycle by triggering and coordinating actions across systems. Agents capture policy changes, initiate renewals, synchronize updates across policy, billing, and claims systems, and ensure that all required steps are completed. They manage dependencies such as recalculating premiums after endorsements and triggering document reissuance upon changes, while routing exceptions and complex cases for manual handling.

Sample agentic workflow

Reported outcomes

Agentic AI can autonomously handle more than 60% of data-heavy policy management workflows that historically required human involvement, such as customer data changing, policy reissuance, and renewal outreach. Insurance offices that adopted agentic automation for policy renewal and change processing achieve the time savings of 4–5 hours per update request while preventing errors and non-compliance.

AI for insurance compliance control

While machine learning engines can handle dynamic compliance controls and violation flagging, GenAI works best for targeted operations such as KYC and due diligence checks and reviewing large-volume documents. AI assistants can help compliance teams draft breach reports and plan risk mitigation. Agentic systems can orchestrate compliance checks, risk escalation, and breach response.

How AI works for compliance control

During customer onboarding and policy changes, LLM-powered engines capture customer and transaction data from submissions and scope compliance-sensitive indicators (identity, ownership, risk, etc.). Following predefined rules, they perform KYC/AML checks against the insurer’s policies and regulatory requirements, screen customers against sanctions lists, and conduct adverse media analysis by reviewing external data sources and public information.

During ongoing operations, machine learning models continuously monitor transactions, payments, and employee activity, detect suspicious patterns indicating non-compliance, and trigger breach alerts. Compliance teams can use LLMs to analyze policy documents, customer interactions, and internal records, highlight and explain compliance gaps, and draft case summaries.

AI agents coordinate and enforce one-time and perpetual compliance controls: initiate customer due diligence checks and enhanced verification for high-risk transactions, collect supporting evidence, trigger activity blocking, and route complex cases to human investigators.

Reported outcomes

By automating high-volume compliance verification and investigation activities across the insurance life cycle, agentic and generative AI technologies help insurance organizations reduce manual compliance effort by 20–40%. Early adopters report 30–60% faster review cycles and up to 60% more accurate compliance assessments. With AI-powered predictive analytics, firms can shift from periodic, reactive compliance checks to proactive, perpetual controls.

Watch Insurance Agentic AI in Action

See ScienceSoft’s Head of AI attempt to justify a “fraudulent” claim — only to be flagged by the AI agent. Built on AWS Bedrock AgentCore and driven by OpenAI’s leading LLMs, the agentic solution can boost investigation efficiency by up to 40% and improve fraud detection rates by over 20% by accurately spotting conversational fraud signals.

Technologies and Tools We Use to Deliver AI for Insurance Companies

Generative AI

Models

- Large Language Models (LLMs)

- Small Language Models (SLMs)

- Multimodal models

- Computer vision models

- Image generation models

- ASR speech models

- TTS speech models

- Audio models

- Real-time

Model adaptation and efficiency

- Fine-tuning

- Instruction tuning

- LoRA adapters

- RAG

- Graph RAG

- Agentic workflows

AI platforms and services

- Azure OpenAI Service

- Amazon Bedrock

- Hugging Face Inference

- Oracle Cloud

- G42/Core42

Agents and Orchestration

- OpenAI Agents SDK

- OpenAI Agents

- AWS Agents

- LangChain

- LangGraph

- smolagents

- LiveKit

- Dify

- n8n

- Faiss

- ChromaDB

- Qdrant

- Weaviate

- OpenSearch

- Pgvector

- Amazon Neptune

- Graph RAG Toolkit

- Neo4j

Traditional ML

Platforms and services

- Azure Cognitive Services

- Azure Machine Learning

- Microsoft Bot Framework

- Amazon SageMaker AI

- Amazon Transcribe

- Amazon Lex

- Amazon Polly

- Google Cloud AI Platform

- Google Vertex AI

Frameworks and libraries

- Apache Mahout

- Apache MXNet

- Caffe

- TensorFlow

- Keras

- Torch

- OpenCV

- Apache Spark MLlib

- Theano

- Scikit Learn

- Gensim

- SpaCy

Standards and regulations we adhere to

NAIC (including AI Principles and Model Bulletin), US state-level regulations (e.g., Colorado AI rules), NIST AI RMF, GLBA, NYDFS, CCPA, HIPAA (for health insurance), GDPR and AI Act (for the EU), IA (for the KSA), SOC 1/2, bank-grade model risk management practices (e.g., SR 11-7), and more.

Security mechanisms we work with

- Data protection: DLP (data leak protection), data discovery and classification, data backup and recovery, data encryption.

- Endpoint protection: Antivirus/antimalware, EDR (endpoint detection and response), EPP (an endpoint protection platform).

- Access control: IAM (identity and access management), password management, multi-factor authentication.

- Application security: WAF (web application firewall), SAST, DAST, IAST (security testing).

- Network security: DDoS protection, IDS/IPS, SIEM, XDR, SOAR, email filtering, SWG/web filtering, VPN, network vulnerability scanning.

Why Engineer AI-Powered Insurance Solutions With ScienceSoft

- Since 1989 in AI consulting and implementation.

- Since 2012 in custom insurance software development.

- Insurance IT and compliance consultants (NAIC, GLBA, NYDFS, HIPAA, GDPR, SOC 1/2, etc.) with 5–20 years of experience.

- 45+ certified project managers (PMP, PSM I, PSPO I, ICP-APM) with experience in large-scale digital transformation projects for Fortune 500 firms.

- Principal architects with hands-on experience in designing complex insurance automation systems and driving secure implementation of AI technologies.

- Established practices to ensure the high quality of insurance solutions and their delivery on the agreed timelines and budget despite project constraints and uncertainty.

ScienceSoft’s clients say

What stood out was ScienceSoft's proactive suggestions for cost-saving architecture design and tech stack solutions. Their input ensured we stayed within budget without compromising on software quality. The value we derived from partnering with ScienceSoft is definitely worth the investment.

Partnering with ScienceSoft has been an excellent experience. They identified and fixed several longstanding issues that had been causing persistent difficulties. Their communication was exemplary; we never had to chase them for updates, and they were always prompt in responding to our queries.

Damien Sewell

Head of IT Projects

Engaging ScienceSoft this way saved us a lot of precious time and resources. Their quick buy-in and readiness to take the initiative made the project faster and less stressful for everyone involved, from Capital IM’s insurance specialists to leadership. We couldn’t have asked for a better IT partner.

Insights From ScienceSoft's Insurance IT Experts

Vadim Belski

Head of AI, Principal Architect, ScienceSoft

Fraud Detection AI Agents: 6 Guardrails for Insurers

Stacy Dubovik

Financial Technology & AI Researcher, ScienceSoft

Interview

Using AI for Financial Planning in Health Insurance

Olga Vinichuk

Insurance IT & AI Consultant and Lead Business Analyst, ScienceSoft

Technology overview

Bringing Smart Underwriting to Health Insurance