Embedded Insurance Software for Carriers

Key Components, Development Options, Costs

With 14 years of experience in insurance IT, ScienceSoft helps carriers engineer tailored product logic, interoperable software architectures, and secure AI components to support embedded insurance models.

Contributors

Senior Insurance IT & AI Consultant, ScienceSoft

Insurance IT & AI Consultant and Lead Business Analyst, ScienceSoft

Embedded Insurance Software for Carriers: Brief Overview

Embedded insurance software refers to the set of technology components carriers need to operate insurance programs through third-party, non-insurance distribution channels, such as ecommerce platforms, fintech apps, travel marketplaces, and mobility services.

Such software can help automate product configuration, underwriting, quoting, policy servicing, and claim handling workflows across embedded distribution networks. A typical carrier-side solution includes product-specific insurance automation logic, partner integration tools, data processing pipelines, and analytics engines.

The cost of developing embedded insurance software may range from $100,000 to $1,500,000+, depending on solution complexity, the degree of component reuse, the chosen approach to logic design, and the scope of integrations. Use our free calculator to estimate the cost for your case.

Technology Components Carriers Need for Embedded Insurance

In my experience, you rarely need to build an entirely new system from scratch to launch an embedded product. Most insurers already have the foundational tools, like underwriting and policy admin engines; you can source the rest of the components from technology vendors, external sales channels, and embedded distribution intermediaries.

The key architectural decision here is which parts you should own and differentiate as a carrier, and which you can delegate to external partners with minimal business risk. It’s less a build-versus-buy question than an ownership-and-control question.

Personally, I’d advise carriers to own the components that define product economics, risk management, and compliance operations. Commodity capabilities like identity verification, document generation, and payment processing are often more cost-effective to procure as services or integrate from third-party providers.

The table below shows where carriers typically need control, where existing systems can be reused, and where third-party services are usually the smarter choice.

Customer trust starts at the point of sale

When evaluating sellers, marketplaces, and embedded insurance platforms, pay close attention to the quality of the customer journey they provide. Does the partner present coverage terms clearly? Does it explain what is and is not covered? Does it allow easy access to policy documents, are claims and support mechanisms transparent? The quality of these interactions directly affects customer trust, conversion rates, and long-term program performance.

Audience reach certainly matters. However, my industry contacts report seeing limited results from high-traffic partners that bury insurance offers in crowded checkout flows, explain coverage poorly, or provide too little context for customers to understand the product's value.

Custom-Built Logic Blocks to Enable Embedded Models on the Carrier Side

Below are the capabilities carriers most often customize when they need control over product economics, risk, compliance, partner operations, and distribution performance. ScienceSoft can develop selected components and integrate them into your existing insurance systems, or engineer a standalone embedded distribution layer.

![]()

Partner onboarding and demand analysis

Partner onboarding pipelines can automate KYB verification, sanctions screening, licensing checks, and contract generation for insurance distribution partners. They create partner accounts with user-defined business specifications, roles, and regulatory constraints. Users can segment partners by industry, jurisdiction, line, and risk appetite and model partner-specific insurance distribution and commission strategies. Demand planning engines can be used to analyze distributor business models, customer segments, transaction flows, and product catalogs, and to forecast time-framed demand for insurance.

![]()

Insurance product configuration

No-code product design tools let insurers configure proprietary embedded insurance products and distributor-specific product variations tailored by line, customer segment, coverage structure, exclusions, limits, eligibility rules, and more. With custom product configuration modules, users can set up unique promotion, submission processing, rating, underwriting, and claim automation logic for each product and apply product-specific data models. Product modeling tools can simulate product- and portfolio-level conversion impacts, loss ratios, and commission scenarios, and run what-if tests for varying coverage parameters.

![]()

Product exposure to distribution partners

A catalog management module can allow users to compose template-based insurance product catalogs with availability tailored by distribution partner, partner cluster, channel, region, and more. The distribution pipelines then automatically expose these catalogs to distributors via versioned APIs and embeddable UI components (e.g., white-label widgets for online partner catalogs and web and mobile checkout interfaces).

![]()

Custom underwriting engines can capture insurance selections within the primary purchase platforms and evaluate risk in real time. For predefined low-risk scenarios, they instantly confirm eligibility and apply standard pricing. For complex cases, the engine can match customer-specific risk attributes against the insurer’s underwriting rules, calculate personalized quotes, and submit them back to the distributor interface. Insurers can apply tailored referral thresholds so the engine routes complex cases for manual review.

![]()

Billing modules automatically separate insurance premiums at checkout, bundle them into total transaction values, or accumulate them for periodic aggregated invoicing to distribution partners. They can calculate taxes, handle refunds, reconcile premiums, chargebacks, and partner balances, and enter transactions into the insurer’s ledgers in accordance with jurisdictional rules. Commission engines calculate distributor compensation based on fixed-percentage, tiered, or performance-based structures, automatically accrue liabilities, and generate payout reports.

![]()

Embedded policy management engines can auto-issue insurance policies upon successful checkout, generate compliant documentation (e.g., COIs, explanations of benefits), register policies in a centralized database, and store contracts in a structured repository. Insurers can build custom policy templates, including multi-language and multi-currency templates, for diverse partners, products, and geographies. The engine tracks policy effective dates, expirations, endorsements, and cancellations, and automates renewal workflows where applicable.

![]()

Claim handling components can automatically aggregate claims across insurer apps and partner platforms. They extract FNOL data, process multi-format claim evidence, and validate claim accuracy and eligibility against policy terms and trusted third-party sources. The module can route valid claims directly to settlement and submit complex cases for manual handling, flag gaps and fraud indicators, and temporarily block claim-associated transactions. A connected payment engine can automate payouts based on insurer-defined models and schedules.

![]()

Custom risk pipelines can be built to continuously monitor insured-produced and third-party risk data (e.g., environmental or telematics streams), detect policyholder-specific and mass exposures, and recalculate risk parameters. They can initiate predefined insurance actions across alternative products, e.g., adjust pricing based on driver behavior for usage-based motor insurance, apply discounts for completed health goals in behavior-based health lines, and trigger payouts when preset risk thresholds are met for parametric programs.

![]()

Tailored analytics engines can calculate, track, and dynamically forecast selected embedded insurance metrics. Users can monitor aggregated sales, underwriting, claims, and financial KPIs across distribution partners via dynamic dashboards and dissect metrics by channel, product version, region, and more using slice-and-dice capabilities. Diagnostic models can identify key drivers of embedded product conversion rates, quote-to-bind ratios, written premiums, loss ratios, commission expenses, and customer retention rates, highlight bottlenecks, and find the root causes of issues.

![]()

Distribution compliance and partner oversight

Compliance engines can continuously monitor partner-driven insurance transactions against the insurer’s policies and relevant regulations (e.g., NAIC, state DOI frameworks, GLBA, the FTC truth-in-advertising rules). They can automatically detect violations of product restrictions, distribution rules, disclosure requirements, consent policies, and data exchange standards (e.g., ACORD, EDI) and generate compliance evidence and reporting packages for internal audit teams, partners, and regulators. A dedicated audit trail mechanism can provide a complete log of embedded insurance activities.

Ways to Implement Proprietary Embedded Insurance Logic

While carriers can often reuse existing systems or use third-party services for embedded insurance infrastructure, API management, and commodity functions (payments, communications, etc.), product-specific business logic typically requires custom engineering.

There are two main approaches to building your own embedded insurance logic, and each has its benefits and limitations. Below, ScienceSoft’s consultants share a high-level comparison of the two.

|

|

Greenfield development |

Brownfield development |

|---|---|---|

|

Essence

|

Building embedded insurance logic into a dedicated platform, independent of the existing core insurance systems. |

Building embedded insurance logic components on top of existing insurance systems. |

|

Pros

|

|

|

|

Cons

|

|

|

|

Best for

|

|

Carriers with modular, cloud-based insurance systems that can accommodate logic extensions and scale with the growing transaction volumes. |

How AI Can Reinforce Embedded Insurance Operations

The Insurance Innovation Reporter predicts a mainstream shift to AI-supported embedded insurance operations in 2026, naming generative AI and multi-task agents the next big value drivers for document validation, eligibility checks, claim adjudication, and customer servicing.

ScienceSoft’s consultants recommend adding AI-supported capabilities across the following embedded insurance tasks:

![]()

Product optimization

Unlike static models, AI algorithms can detect non-obvious demand patterns like changes in browsing depth, elasticity shifts, cart modifications, time-of-day dynamics, and cross-product affinities. They can continuously assess the impact of these signals on expected conversions and suggest refinements to product structures.

![]()

Dynamic product personalization

AI-based recommendation engines can spot trends in customer-level behavior, distributor transaction data, and sales performance, match them to insurance product attributes, and dynamically suggest coverage structures and price points that are most likely to convert for individual customers and specific transaction types.

![]()

Submission processing

Large language models (LLMs) and image analysis tools can parse multi-format applications and claims documents, extract structured data, and validate submission consistency and completeness in near-real time. Underwriters can use LLMs to draft structured explanations and customer messages for eligible cases and adverse decisions.

![]()

Fraud detection

Although distribution partners typically perform basic fraud screening, carriers may add AI-powered fraud detection tools to independently vet the received information. AI tools can check partner-submitted data for anomalies and identify sophisticated fraud patterns, including document tampering and AI-generated IDs or claim evidence.

![]()

Distributor risk prediction and mitigation

Machine learning engines can detect subtle indicators of deteriorating partner portfolio quality, such as unexpectedly high loss ratios, unusual claims patterns, or elevated cancellation rates across particular distributors. They can alert insurers to emerging partner risks and recommend corrective actions, such as modifying pricing models or strengthening customer education measures.

![]()

End-to-end workflow automation

During purchasing, AI agents can capture transaction data from a distributor platform, retrieve product rules, evaluate eligibility, trigger premium calculation, generate a quote, and return the offer to the checkout interface. After purchase, the agents can issue the policy, register the contract, and trigger bill and commission calculations — all in alignment with the carrier’s process rules and human-in-the-loop controls.

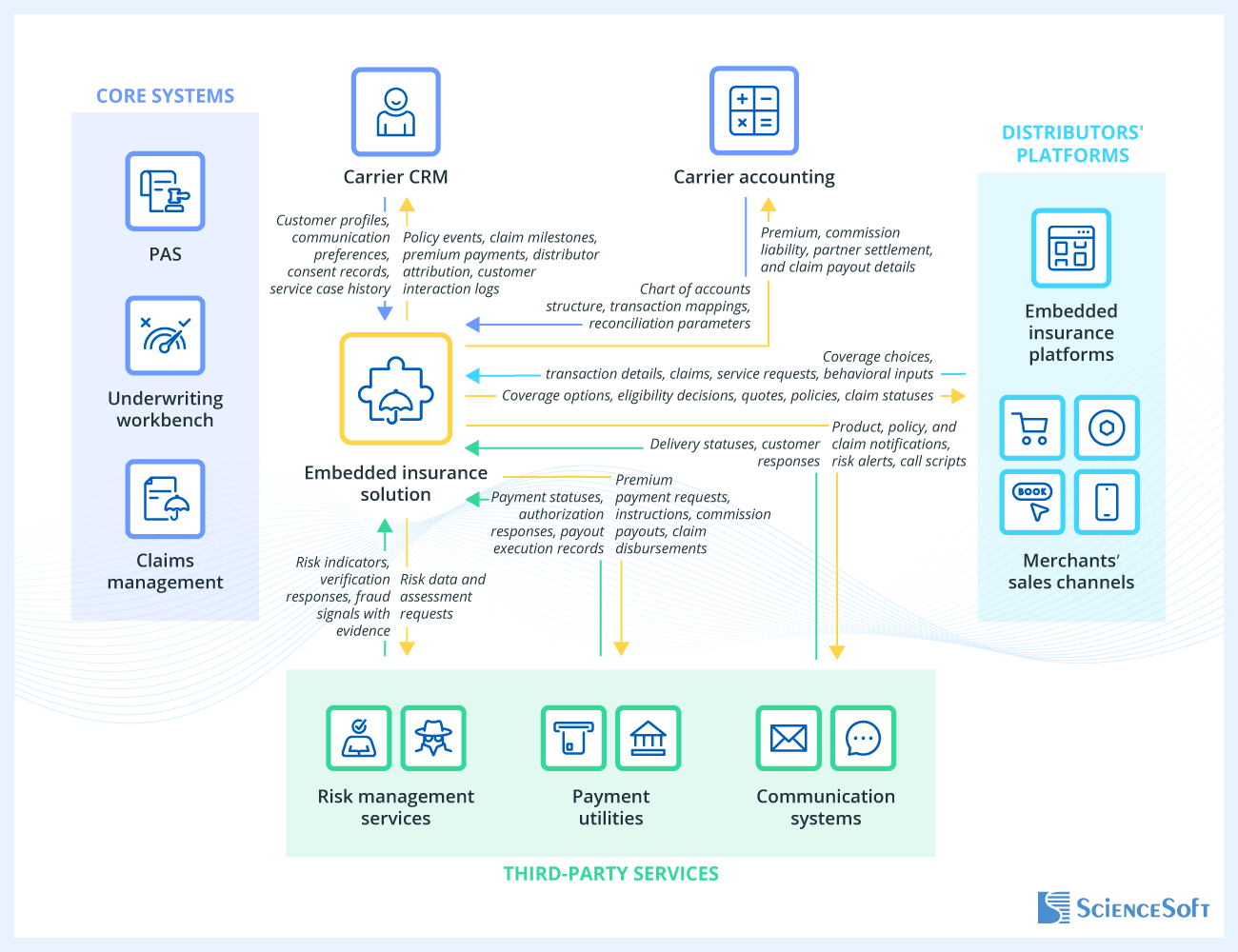

Essential Integrations for Embedded Insurance Systems

- Distributors’ platforms (e.g., embedded insurance platforms, merchants’ sales channels (ecommerce apps, fintech apps, travel booking systems, mobility services) — to enable real-time underwriting and quote exposure during checkout and speed up policy servicing and claim intake.

- Third-party risk management services (e.g., identity and AML/OFAC verification services, fraud intelligence platforms) — to streamline KYC/AML and eligibility screening and accurately detect fraud during underwriting and claim processing.

-

Payment utilities (e.g., payment gateways, payment processors, banks’ systems) — for automated premium collection at checkout, fast claim payouts and commission disbursements, and reconciliation of distributor and payment processor settlements.

-

Communication systems (e.g., email, SMS, and instant messaging services; call center and IVR systems) — for quick omnichannel communication with insurance customers.

-

Insurance accounting software — to automate insurance transaction posting into accounting ledgers, simplify financial reconciliation across embedded transactions, and maintain accurate premium and commission accounting.

-

Insurer’s CRM — to maintain a unified customer view across embedded channels, enable coordinated service and cross-sell strategies, and trigger outreach at policy and claim milestones.

Best Practices for Embedded Insurance Software Development

Below, ScienceSoft’s experts share their best practices for engineering reliable and cost-effective embedded insurance solutions.

![]()

API orchestration streamlines partner onboarding and integration maintenance

Without a dedicated integration layer, insurers typically need to build and maintain separate integrations for each distribution partner and embedded insurance platform they work with. As partner networks grow, every new integration would require custom mapping of customer and insurance data and separate maintenance whenever either side changes its APIs.

ScienceSoft's architects recommend implementing an API orchestration layer between the carrier’s embedded insurance solution and partner systems. This layer can manage authentication, traffic routing, API version updates, and other integration tasks in a single place. It can also automatically translate partner-specific data formats into the formats used by the insurer's underwriting, policy administration, claims, and analytics engines.

As a result, insurers can onboard new distributors and intermediaries faster, reduce integration maintenance effort, and scale embedded insurance programs without creating dozens of partner-specific connections.

Well-documented APIs minimize integration errors

Clean API specifications, schemas, authentication rules, and versioning policies reduce ambiguity in API usage and help minimize integration issues. At ScienceSoft, we prioritize API documentation during engineering and stick to standardized formats like OpenAPI. This approach accelerates API SDK design and makes integration guidelines more friendly for insurers’ and partners’ IT teams.

![]()

Configurable data flows support compliant business scaling without costly rework

In embedded insurance, the biggest compliance risk is sensitive data movement between the carrier and its partners. If these flows are designed solely for an initial partner or distribution model, the carrier will need to reengineer integrations, access controls, audit trails, and data pipelines when expanding into new channels, jurisdictions, or product lines.

ScienceSoft recommends mapping the expected data flows at early design stages: what data each party sends or receives, where it is stored, who can access it, how consent and disclosures are recorded, and which events must be auditable. Since future partners may have different data-sharing models and compliance obligations, controls for consent management, disclosure evidence, retention periods, access rights, and regional data storage should be configurable. This allows insurers to onboard new distribution partners and enter additional markets without creating separate compliance processes.

![]()

Modular cloud architectures work best for gradual and situational scaling

Embedded insurance platforms must handle both gradual expansion of distribution partnerships and sudden spikes in transaction volumes during partners’ promo campaigns, seasonal sales events, and high-traffic claim flows during mass-risk events. Cloud-based modular architectures allow you to independently scale computing resources for specific platform components (policy issuance pipelines, pricing services, or claim processing modules) as demand grows. Selectively applied serverless functions and event-driven messaging can further support spiky workloads by automatically scaling infrastructure during high-volume partner and claim transactions while minimizing idle capacity during normal operations.

Costs of Embedded Insurance Software Solutions

Developing embedded insurance software may cost from $100,000 to $1,500,000+, depending on the solution’s functionality, the scope of supported product lines and jurisdictions, the number and complexity of integrations, as well as performance, scalability, and security requirements.

Here are ScienceSoft’s sample cost ranges for common development scenarios. These ranges cover the design and implementation work and exclude third-party component licenses, network fees, cloud hosting, and AI model usage:

![]()

$100,000–$200,000

A small-scale MVP for an embedded insurance solution, focused on one product and one distribution partner. Typically, it would feature one API, a standard quote-bind-issue workflow, a consent capturing pipeline, and status syncing capabilities.

![]()

$150,000–$400,000

A custom logic module that supports a specific embedded insurance function (e.g., underwriting, quoting, claim processing, claimant self-service). The module features rule-based automation and can be extended with AI capabilities.

![]()

$500,000–$1,500,000+

An enterprise solution handling the entire scope of embedded insurance activities, including product optimization, risk management, and analytics. It can include a multi-partner orchestration layer and feature rule-based and AI-supported automation.

Wondering how much your software project will cost?

Use our online calculator to describe your needs, and we'll get back to you shortly with a tailored estimate. It’s free and non-binding.

* The estimates are for midsize organizations (<2,000 employees) serving 1–3 major embedded insurance lines. The final implementation cost will depend on the insurer’s specific needs and the maturity of the firm’s IT ecosystem.

Embedded Insurance Technology Market Trends and Business Impact

The World Economic Forum predicts that by 2028, more than 30% of all insurance transactions will run through embedded channels. BCG’s 2025 findings show that total gross written premiums from embedded insurance can grow by over 430% by 2030. Insurers themselves are also confident in the growth trajectory: according to SAS, 59% of carriers expect their embedded business to grow by 5–20% in the near term.

Insurers favor embedded models primarily for access to a broader customer base at a fraction of direct customer acquisition costs. Embedded products are particularly appealing to younger and gig economy segments: 84% of such consumers prioritize insurance options integrated into digital sales channels. In the long term, embedded insurance can also help carriers boost customer engagement and brand awareness.

The embedded insurance model has proven financially viable: according to a carrier survey conducted by SAS and the Open and Embedded Insurance Observatory, 70% of adopters confirm its positive business impact, and 35% report annual written premiums of $100+ million from embedded products, with 29% of those reporting premiums of $200+ million.

Why Build Embedded Insurance Software With ScienceSoft

- Since 2012 in engineering custom software solutions for the insurance industry.

- Practical knowledge of 30+ industries to create embedded insurance solutions that fit the specifics of distribution partners from diverse domains (ecommerce, telecoms, automotive, and more).

- Insurance IT and compliance consultants with 5–20 years of experience and expertise in insurance regulations (NAIC, state DOI rules), data exchange and interoperability standards (incl. ACORD data models and messaging standards), and data protection frameworks (NYDFS, CCPA/CPRA, GLBA, HIPAA, GDPR).

- 45+ certified project managers (PMP, PSM I, PSPO I, ICP-APM) who succeeded in large-scale projects for Fortune 500 firms.

- Principal architects with hands-on experience in designing complex insurance automation systems and driving secure implementation of emerging technologies.

- 350+ software engineers, 50% of whom are seniors or leads.

- Established practices to ensure the high quality of insurance solutions and their delivery on the agreed timelines and budget, despite project constraints or uncertain requirements.

ScienceSoft’s clients say

ScienceSoft are responsive, technically sharp, and they communicate well with our people. When we've needed to move fast, they've stepped up and delivered. What I appreciate most is their proactive approach. They don't just wait for us to identify issues. They bring solutions to the table and help us prioritize what matters most. That kind of partnership is hard to find.

Partnering with ScienceSoft has been an excellent experience. Their team transformed our underwriting platform into a well-oiled machine. They identified and fixed several longstanding issues that had been causing us persistent difficulties. Their communication was exemplary; unlike our previous experiences with outsourcing, we never had to chase them for updates, and they were always prompt in responding to our queries.

Damien Sewell

Head of IT Projects

ScienceSoft’s quick buy-in and readiness to take the initiative made the project faster and less stressful for everyone involved, from Capital IM’s insurance specialists to leadership. At the end of a short yet highly productive two months, we got a secure and wholly owned property insurance solution that is fully adapted to Capital IM’s corporate practices and brand book. We couldn’t have asked for a better IT partner.